“It is a comfortable feeling to know that you stand on your own ground. Land is about the only thing that can’t fly away.” (English novelist Anthony Trollope)

With interest and home loan rates at their lowest since 2022, it’s no surprise that South Africa’s property market confidence level at the end of 2025 was sitting at a record high of 87%. That will have been boosted by the country’s positive economic outlook following Budget 2026, and by Budget 2026’s 50% increase in the primary residence exclusion (which should stimulate sales by reducing the CGT payable by sellers).

If you are a buyer about to put in an offer on a house, remember to budget for the various costs you’ll face over and above the purchase price. In all the excitement of your purchase (particularly if it’s your first house!) it’s easy to underbudget. But you really don’t want to risk any unpleasant financial surprises. If you do breach a term of the sale agreement by not paying something on time, you could even face cancellation of the sale and a damages claim.

Only with a proper budget and cash flow forecast can you be confident both that you really can afford to offer for the house you’ve fallen in love with, and that you’ll be able to pay everything you need to, when you need to.

Have a look at the list we’ve put together below and use it to prepare your own detailed cash flow forecast. Ignore anything that doesn’t apply to you and bear in mind that every buyer’s situation will be unique, so this is no more than a generalised checklist.

Costs payable before transfer

- The deposit: Most sale agreements – often titled as an “Offer to Purchase” (OTP) until it’s accepted by the seller – require you to pay a deposit, usually 5% or 10% of the purchase price.

- Bond/home loan initiation fee: This fee normally incorporates a valuation fee and is added to your loan, but check with whichever bank you use.

- Homeowner’s insurance policy and life cover policy (if required by the bank): Be sure to provide for payment of the first premiums before bond registration.

- Balance of the purchase price: If the deposit you paid and the bond you took out don’t cover the full price, you’ll need to pay the balance before transfer.

- Transfer duty: Unless VAT applies to the sale, transfer duty is payable. This is a government tax payable via SARS before transfer. It applies to all property sales over R1,210,000, on a sliding scale linked to the sale price. This can be a substantial cost!

- Transfer fees: The transferring attorney (conveyancer) charges fees based on a sliding scale linked to the sale price. Added to the account will be charges for FICA verification, deeds searches, postages and petties, other disbursements and the like.

- Bond registration fees: If you take out a bond, the bank appoints an attorney to register it, with the fees calculated on the size of the loan and including the attorney’s fees, FICA charges and a prescribed Deeds Office registration fee.

- Deeds Office fees: These are government charges for both transfer and bond registration.

- Rates clearance: Your local municipality will require advance pro-rata payment of municipal rates before it issues the necessary clearance certificate.

- Levy clearance: Similarly, if you are buying into a complex, the sectional title’s body corporate or Homeowners’ Association (HOA) will require pro-rata levy payments before issuing a clearance certificate.

- Occupational interest (if applicable): If you take occupation before transfer, you need to budget for whatever occupational interest is provided for in the sale agreement.

- Utility deposits: If required by your local municipality when opening up water and electricity accounts.

- Moving costs: Don’t overlook these when budgeting!

Some of these costs are easily overlooked, but they can add up alarmingly. So, plan for them all before you put in your offer to purchase.

Ongoing monthly costs after transfer

Include bond instalments, municipal rates and taxes, levy payments (if you buy in a sectional title or HOA), utility charges, insurance premiums for the property and the contents, and so on.

One-off costs after transfer

If you plan to do alterations or repairs, redecoration, garden revamps, furniture replacement or anything similar, add these costs to your budgeting so you don’t suddenly run out of money and have to postpone them. For long-term planning, set aside a budget for ongoing home maintenance.

As always, we are here to assist, so let us know if you have any questions, need any further information, or would like help in creating a cash-flow projection specific to your purchase.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“Knowledge is power.” (Sir Francis Bacon)

Being a company director carries not only rewards but also risks that you need to manage carefully.

In particular, you are held by the Companies Act to a high standard of conduct. Breaching any of your many duties and responsibilities can have significant negative consequences. Among these is being declared a “delinquent director”. That’s no small thing…

It’s a serious long term career risk

Serious categories of misconduct expose directors to being declared delinquent and thus disqualified from holding any directorship or senior management position for a period ranging from 7 years to a lifetime.

A wide range of less serious categories of misconduct can lead to “probation” orders, with possible consequences including disqualification for up to 5 years, supervision by a mentor, remedial education, community service, and payment of compensation.

The other side of the coin, of course, is that the delinquency risk isn’t just a warning to directors. It also gives victims of director misconduct a powerful remedy.

Let’s illustrate in the context of two recent cases.

Seven years in the wilderness (and a R78m damages bill) for a delinquent MD

Two groups of granite producing companies, one responsible for quarrying and the other for production and export, operated inter-dependently for decades. All went well until the Managing Director of the quarrying group of companies placed them into business rescue. Unsurprisingly, this had a devastating effect on both groups, with mining rights in jeopardy, credit lines and bank facilities lost, production levels affected, discussions with SARS over penalties terminated, and millions wasted both in the business rescue process and in remedying the aftermath.

The companies in the surviving group of companies sued the MD of the quarrying group with allegations that those companies should not have been placed into business rescue at all, and for various other acts of mismanagement and misconduct.

The MD’s defences to these claims found no favour with the Court, which declared him delinquent and ordered him to pay R78m in damages. He had, the Court held, unnecessarily placed companies into business rescue without engaging shareholders and despite available shareholder support and the absence of true financial distress. He had acted with gross negligence, caused substantial financial damage, breached his fiduciary duties (i.e. used his powers improperly and not in the best interests of the companies), and neglected his supervisory duties relating to quarry operations.

Another director, another disqualification

Now let’s move to a struggle between two shareholder factions for control of an investment company with energy sector interests. Exasperated, one faction went to the High Court to challenge the validity of a board resolution and share issue which affected their control of the company. There was substantial value at stake here, possibly (reading between the lines of the judgment) many millions of US dollars.

The dispute eventually found its way to the SCA (Supreme Court of Appeal), where, on application by the opposing shareholder faction, a director (and sometime Executive Chairperson) of the investment company was declared delinquent for seven years.

He had, found the Court, acted with gross negligence, wilful misconduct and breach of trust in performing his functions. Here’s one example among many: even after his removal as Chairperson, he purported to call a shareholder meeting “By order of the Chairman.” That alone, said the Court, was “a blithe disrespect for corporate governance and [a breach of] his fiduciary duty as a director.”

If you’re a director, here’s how to manage your risk

Your best defence against hostile stakeholders will always be to remain fully aware of all your many fiduciary duties, and to scrupulously comply with them. Knowledge is power!

Act early to address any financial issues that could lead to accusations of reckless trading or of causing financial harm to the company. Ensure that proper financial and operational controls and procedures are in place. At all times act strictly in the best interests of your company with transparency and good faith, proactively exercise proper oversight of all operations, and – perhaps most importantly – ask us for advice if in any doubt!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“The only man who sticks closer to you in adversity than a friend is a creditor.” (Evan Esar)

Body corporates face a familiar problem. Owners fall into arrears. Levies go unpaid. Legal costs mount. The temptation is to reach for the most forceful remedy available.

Sequestration may seem like that remedy. If an owner will not pay, why not have them declared insolvent?

A recent Gauteng High Court judgment offers a clear warning. A body corporate sought the sequestration of a unit owner for levy arrears exceeding R1.4 million. With such a substantial debt, the body corporate’s frustration was understandable. But the application failed.

The court held that the body corporate had not met the statutory requirements under the Insolvency Act. In particular, it had not shown that sequestration would be to the advantage of creditors. The court also noted that the body corporate had other execution remedies available and emphasised that sequestration proceedings are not intended to function as a debt-collection mechanism.

What is sequestration?

Sequestration is a court-ordered insolvency process under the Insolvency Act. It applies where a debtor can no longer meet their financial obligations. The court places the debtor’s estate under the control of a trustee, who sells the debtor’s assets and distributes the proceeds among creditors.

The test for sequestration

To succeed, the applicant must establish three things:

- The debtor has committed an act of insolvency, or is actually insolvent.

- There is reason to believe sequestration will be to the advantage of creditors.

- The applicant has a liquidated claim against the debtor.

The second requirement is where many applications come unstuck.

Where sequestration applications unravel

Sequestration is not designed to punish debtors or pressure them into payment. It’s a collective remedy, intended to ensure the orderly distribution of a debtor’s assets among all creditors.

The applicant must prove that there’s a good chance that creditors will receive a meaningful dividend. If the debtor has no realisable assets, or if the costs of sequestration would consume whatever value exists, the application will fail. The court will not grant sequestration simply because a debt is owed.

Sequestration is not leverage

In practice, some creditors use sequestration applications as a form of pressure. Their reasoning is simple: the threat of insolvency may prompt the debtor to settle. But our courts have made clear that this is not appropriate.

In this case, the court emphasised that insolvency proceedings are not a private debt-collection mechanism. They carry serious consequences: loss of control over assets, restrictions on legal capacity, and reputational harm. These consequences are justified only where the statutory purpose is served.

Where the true aim is to recover a debt rather than administer an insolvent estate, the court will refuse the application.

What body corporates should consider

Before pursuing sequestration, a body corporate should ask practical questions.

- Does the owner have realisable assets? If the only asset is the unit itself, and it is bonded, there may be little left after the bondholder is paid.

- Would the costs of sequestration exceed the likely recovery?

- Has the body corporate exhausted more conventional remedies? A judgment, followed by execution against property, may be more direct and effective.

If the answers suggest that sequestration will not benefit creditors, the application is unlikely to succeed.

Other options

Body corporates have several remedies for levy recovery: obtaining a judgment and executing against the property, applying for an attachment of emoluments, or seeking a sale in execution.

Each has its own requirements, but they are all designed for debt recovery (unlike sequestration).

Where this leaves body corporates

Sequestration is a remedy of last resort, not a debt-collection tool. The Insolvency Act sets strict requirements, and courts will hold applicants to them. If you are unsure which remedy is appropriate, we can help.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“Legacy is not leaving something for people. It’s leaving something in people.” (Peter Strople, former Dell Computer Corporation director)

Leave a personal legacy, not just a financial one

We all know how important it is to our loved ones that we leave behind a valid will rooted in a comprehensive estate plan, but our legacy should go a lot further than just distributing assets.

Sharing with your heirs your values, your family history, and the wisdom your years have granted you can be one of the most important gifts you leave, often outlasting tangible bequests by generations. On a practical level, it will also help your heirs value, preserve and enjoy the wealth and the heritage that you leave them.

Start with a family mission statement

This sounds very corporate and complicated, but in fact it’s really simple and entirely personal. A family mission statement is foundational in legacy planning and will help everyone focus on the values and priorities important to them. As Stephen Covey (author of The 7 Habits of Highly Effective People) puts it “A family mission statement is a combined, unified expression from all family members of what your family is all about – what it is you really want to do and be – and the principles you choose to govern your family life.”

Of course, the mission statement must be collaborative, and everyone, even young children, can share in putting it together. You never know who will come up with a bright idea or two!

There’s a useful downloadable worksheet here if you need help getting started – personalise it to your family’s situation, and adapt it as you go along.

Share and discuss your plans

Openly sharing and discussing your estate planning and the provisions of your will with your nearest and dearest isn’t just an opportunity to prepare everyone for the financial implications of your death. It’s also a great way to involve everyone in your planning and to ask for their input.

Discuss the financial structures you have already put in place, or are planning for the future. Talk about your vision for the wealth you will leave behind and why you have made the bequests you have. Sharing all that, and relating it all to your family mission statement, will significantly reduce the risk of unhappiness and disappointment when the time comes for your last wishes to be implemented.

Craft your “legacy letter”

This isn’t your will (although it’s sometimes misleadingly referred to as an “ethical will”).

What’s the difference? Your formal will, which must comply with all legal formalities to be valid, sets out who is to inherit what from you. In contrast, your legacy letter is an informal and personal letter from you to your loved ones, sharing with them whatever you think will be of value to them in their lives. It needn’t be just one letter – many people choose to write individual letters to each member of their family.

There’s a lot to be said for sharing all these things informally with your family while you are still around, but don’t stop at verbal discussions. Writing them down and leaving them in letter form will give your heirs a permanent point of reference.

What should you include in your legacy letter? Really, anything that you think will help your loved ones live richer and more fulfilling lives. Perhaps share some of your family history, stories of your own life and the lessons it has taught you, your values, and your hopes and dreams for each of them. What challenges have you faced and how did you overcome them? What was really important to you at each life stage? What are your most cherished memories? What stories and advice from your parents and grandparents really helped you? What principles have inspired your financial successes?

The Confucian advice to “Study the past if you would define the future” rings as true today as it did two and a half thousand years ago.

A practical five-point plan brings it all together

- Your estate plan underpins everything, so review and update it regularly.

- Take legal and tax advice on forming a family trust. Depending on your circumstances and objectives, it could be the perfect way of guaranteeing that the financial part of your legacy is protected and managed wisely for generations to come.

As to the more personal side of your legacy, the trust’s name itself will preserve your family name no matter how many of your descendants may in due course acquire new surnames.

- Most importantly, leave behind a valid and updated will (“Last Will and Testament”) that clearly reflects your wishes and complies with all legal formalities.

- To accompany your will, put together a “Notes for my executor and loved ones” file with all the information and documents that your executors and heirs will need when the time comes.

- Last but certainly not least, be sure to include your legacy letter. This ensures that you aren’t just leaving your family all your worldly wealth, but also a real legacy – your own personal message for the future, direct from you to them.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

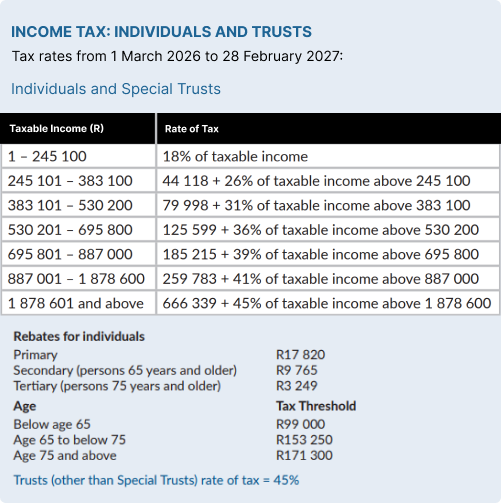

“We are also proposing additional tax measures to ease the financial burden on households and businesses, by adjusting personal income tax brackets and rebates fully in line with inflation.” (Minister of Finance Enoch Godongwana)

How much will I save if I sell my house?

A big highlight for property sellers and buyers is that, having remained unchanged since 2012, the primary residence exclusion for Capital Gains Tax has been increased from R2 million to R3 million. In addition, the annual CGT exclusion has been increased for individuals by 25% from R40,000 to R50,000, and for deceased estates by 47% from R300,000 to R440,000.

The big win is that when you sell your primary residence (the home you live in), the first R3 million capital gain is now excluded from CGT.

Have a look at the illustrative savings calculation below:

Primary residence CGT exclusion: R2m vs R3m

Transfer duty threshold unchanged

Unchanged from last year, you pay no transfer duty if the property you are buying sells for at (or below) the set threshold of R1,210,000.

“Bracket creep” relief for taxpayers

Individual taxpayers:Your tax rates (and the associated rebates and medical tax credits) are increased in line with inflation. That’s welcome relief after last year’s unchanged tax tables which resulted in “fiscal drag” (also referred to as “bracket creep”) for anyone receiving a salary increase that pushed them into a higher tax bracket.

Trusts: Special trusts are by and large taxed as individuals, but other trusts are taxed at a flat rate of 45% – also unchanged from last year.

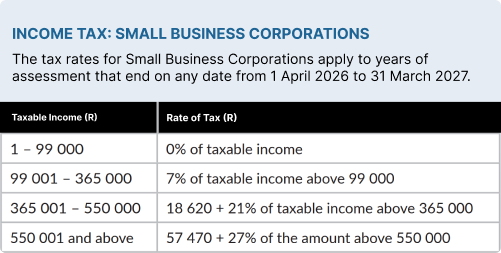

Corporate taxes: The tax rate for companies remains unchanged, with substantial relief for smaller businesses.

“Sin taxes” up: The details

Most sin tax increases were generally in line with or slightly below inflation. See the table below for full details.

Table 4.8 Changes in specific excise duties, 2026/27

Source: National Treasury (Table 4.8)

How much more or less will you be paying in income tax, petrol and sin taxes?

Use Fin 24’s Budget Calculator here to find out.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“Lemon law, noun – a law that states that you can return a motor vehicle to get it repaired or your money back if the vehicle is no good.” (Oxford Learner’s Dictionaries)

The car you just bought on instalment sale turns out to be a complete lemon. But when you return it to the dealership and cancel the sale, the bank still enforces the finance agreement and sues you for damages.

“Sorry to hear about the defects,” says the bank. “But that’s not our problem. We weren’t the supplier; we just financed the transaction. Your claim is against the dealership. You’re still bound by the instalment sale agreement and must cover our losses.”

Sued by the bank after buying a dud 4×4

A motor dealership in Koster (a small farming town in the North West Province) sold a 5-year-old Ford Ranger 3.2 TDCI 4×4 automatic to a mother, who bought it on behalf of her son with bank financing on an instalment sale basis.

All pretty standard stuff… Until, just four days after delivery, the oil cooler and gearbox started giving problems. The son returned it to the dealership, which replaced the gearbox. But then less than two months later, the vehicle overheated. Unsurprisingly the son returned it to the dealership as a dud that he no longer wanted. His mother, as buyer, formally cancelled the agreement with a lawyer’s letter.

The bank sued her for damages, and while it was successful in the High Court, the SCA (Supreme Court of Appeal) reversed that decision and upheld the buyer’s counterclaim for cancellation of the instalment sale and restitution of everything she had paid the bank. The bank must accordingly refund her the deposit and all the instalments she had paid it, together with interest and costs.

That outcome, and the SCA’s reasoning in reaching it, hold important lessons for all suppliers of goods of all kinds (not just vehicles), buyers, and banks.

When you buy a lemon, here’s how to make lemonade

The buyer’s success hinged on the Court’s findings that:

- The vehicle was seriously defective (probably because the incorrect gearbox had been fitted after an accident) and therefore unfit for its intended purpose.

- The defects were “latent”: hidden problems not visible on inspection.

- The buyer was entitled to rely on the “redhibitory action” (actio redhibitoria to lawyers), an old remedy that allows you to cancel a sale of defective goods, return them to the seller, and claim your money back. You will have to show that the defects existed at the time of sale, and that you, acting reasonably, wouldn’t have bought the goods had you known of the defects.

- The fact that the buyer had allowed the dealership to attempt repairs did not affect her right to cancel because it didn’t amount to a waiver (abandonment) of her rights.

- The Consumer Protection Act (CPA) generally requires consumers to exhaust all alternative dispute resolution remedies (such as referring complaints to the applicable Ombud) before going to court. In this case, however, because the bank had already sued the buyer in the High Court, she could raise her counterclaim as part of the same proceedings without first approaching an Ombud.

- Although the finance agreement itself fell under the National Credit Act (NCA), the vehicle (the goods) was still protected by the CPA – and that, as we shall see below, was critical to the outcome here.

- Equally importantly, the bank was not, as it argued, merely the financier. The wording of its own agreement showed that it acted as both the credit provider and the supplier.

- That’s a critical finding, because as “supplier” of the vehicle, the bank was subject to the CPA’s consumer protections, including the requirement that goods must be fit for purpose, of good quality, and free of defects.

Precedent setting?

After this far-reaching decision banks can no longer say “sorry, we just financed the deal, you must sue the seller”. Of course, any banks with differently worded agreements might still be able to argue that they really were nothing more than the finance providers, but banks generally will no doubt take steps now to mitigate this new risk. Perhaps we can expect much tighter lending restrictions or reworded finance agreements? Time alone will tell what they come up with.

For now, though, whether you are suing the seller or the bank to get your money back, your position will be a strong one if you can prove all the above factors.

Act quickly!

As a final cautionary note, the Court made it clear that you must act (i.e. cancel the sale and return the goods) within “a reasonable time” after discovering the defects.

So don’t delay. If you find out you bought a lemon and the seller refuses to cancel the sale and refund you, call us immediately.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“Fraud unravels property transactions even where innocent third parties are involved.” (Extract from judgment)

Congratulations, you’re the proud new owner of your dream home! Your name’s on the title deeds, and your ownership is registered in the Deeds Office. That’s conclusive proof that the house is yours, right? Regrettably, this isn’t always the case…

Although registration is usually proof of ownership, there are exceptions. One exception is fraud. And a recent High Court case is a sharp reminder to every party to a property sale and transfer (seller, buyer, estate agent, conveyancer and bonding bank) that any sale and transfer tainted by fraud will almost certainly unravel.

As we shall see, a crooked “conveyancer” was at the heart of this particular saga, so perhaps the most important lesson here is one for sellers. Choose your conveyancer with care!

A crooked “conveyancer” defrauds both seller and buyer

Many of the facts in this convoluted story were in dispute, but the Court’s decision rested on these findings:

The owner, since 2011, of a house in Bloemfontein lived there with her elderly mother. She signed an agreement in 2020 to sell it for R300k to a trust. The sole trustee’s wife was an attorney, but not a qualified conveyancer. Nevertheless, she was appointed in the sale agreement as the “conveyancer” to attend to the transfer.

Shortly after signing the deed of sale, the owner changed her mind and said she was cancelling the sale. Although her “cancellation” seems to have been accepted by the trust, it was invalid for lack of being recorded in writing and signed. What her attempt at cancellation did prove was that she no longer had any intention of passing transfer to the trust. Moreover, the whole sale agreement fell through when the trust failed to get a bond as required by the bond clause. In the end, the owner received not a cent of the R300k, and presumably she spent the next three years happily confident that the sale had fallen away.

Imagine her shock when in 2023 she received an eviction application from a couple who had, without her knowledge, bought the house from the trust for R480k. Only then did she find out that the trustee and his attorney wife had secretly transferred her house, in consecutive transfers on the same day in 2022, firstly from her to the trust, and then from the trust to the couple. The couple were of course now convinced that the house belonged to them.

Off went our original owner to the High Court, which held that there was no doubt that the husband-and-wife team of trustee and attorney had acted in cahoots to defraud both the original owner and the eventual buyers. It accordingly declared both sales and transfers to be invalid and ordered the house to be re-transferred to the original owner.

Fraud unravels all

At the heart of the Court’s decision lies the old Roman concept of fraus omnia vitiat or “fraud unravels all”. There are some exceptions to the application of this principle in our modern law, but the general rule remains that where a property sale is tainted by fraud, any purported sale or transfer of ownership resulting from it is null and void.

Moreover, one can never pass on to another person more rights than one has. Since the sale to the trust was void, all subsequent sales must also be void regardless of registration of transfer. In any case, the second sale agreement had lapsed, again because of non-fulfilment of a bond clause.

For all those and a variety of other reasons, the original owner had never lost her ownership despite the transfers being registered in the Deeds Office.

The couple who bought the house for R480k must now presumably carry on paying their home loan instalments despite having no asset to show for it, and will be wondering whether they can recover their losses from anyone.

Everyone’s at risk, innocent or not

As the Court put it: “Fraud unravels property transactions even where innocent third parties are involved.”

- Innocent or not, the seller might have lost her house had she been found to have enabled the fraud.

- The buyers, despite being innocent of any fraud, did lose their house. They also have to pay legal costs (the Court criticised their delay in pursuing transfer and in finding out about the occupants) and have no guarantee of getting their money back from anyone.

- Even the estate agents and the bank might have found themselves accused of negligence, perhaps for failing to inspect the house and asking the occupants about the basis for their occupancy. Had they done that, they would have uncovered the fraud.

Bottom line is this: Sellers, don’t take chances when choosing your conveyancer!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

The National Minimum Wage (NMW) for each “ordinary hour worked” has been increased from 1 March 2026 by 5% from R28,79 per hour to R30,23 per hour.

Domestic workers: Assuming a work month of 22 days x 8 hours per day, R30,23 per hour equates to R241,84 per day or R5320,48 per month. Of course, this is just the bare legal minimum. The Living Wage calculator will help you check whether you are actually paying enough to cover a household’s “minimal need” (adjust the “Assumptions” in the calculator to ensure that the figures used are up-to-date).

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“All you need is love… and a good lawyer.” (Anonymous)

February, with its Valentine’s Day chocolates, roses and declarations of undying love, should be a month for romance, not legal niceties. But in the real world, love and the law are inextricably linked because any relationship’s structure and consequences are inevitably governed by legal principles. Losing sight of that can expose you to unnecessary angst, dispute, and litigation.

A recent High Court fight between an estranged couple over their jointly-purchased dream house illustrates this neatly.

Broken dreams, and a fall out over the house

A couple’s four-year romantic relationship saw them living together first in her mother’s house and then in his apartment. They then decided to buy a house together with the idea of making their relationship more permanent.

Unfortunately, that dream came to nought – their relationship ended a month after the property purchase, leaving only one of them to live in the house and to pay all the ongoing costs while they decided what to do next.

In due course they fell out over how to end the co-ownership and how to adjust their respective claims for past and future property costs.

Their dispute reached the High Court, which ordered firstly that the co-ownership be terminated. This was necessary, because no co-owner can be forced against their will to remain a co-owner where the relationship between the co-owners has deteriorated to such an extent that it can’t continue.

Then, using an old Roman law remedy still in use today (the “actio communi dividundo”) the Court dealt with both the division of the property, and the adjustment of the various financial claims between the parties. As is usually the case, these were complex and intertwined after years of cohabitation.

Importantly, the Court noted a modern move away from the traditional principle that the property should necessarily be sold by public auction to the highest bidder, towards a much more flexible approach based on the Court having a wide discretion to ensure a fair and practical outcome in each case.

Thus, having considered all the circumstances, wishes and claims of both parties, the Court ordered that the ex-partner living in the house has a first option (valid for 60 days) to buy the other’s half share at valuation. If he doesn’t, he must offer it for sale on the open market at a fair and reasonable market-related price. If there’s still been no sale after 6 months, the Sheriff of the High Court becomes a “receiver and liquidator” and has 4 months to auction the house. The bond, costs and parties’ related financial claims will be settled from the proceeds as directed by the Court.

“Co-ownership is the mother of dispute” – But it needn’t be

“Co-ownership is the mother of dispute” (“communio est mater rixarum”) is another old Roman law concept mentioned by the Court. It confirms that joint ownership has always, since ancient times, inherently provided fertile ground for instability and dispute.

But that needn’t be so. An upfront agreement between joint owners, whether their arrangement is grounded in a commercial or a personal relationship, can hugely reduce the risks of later uncertainty, disagreement and litigation.

Put as much detail into your agreement as you can, including a detailed process of how to end your co-ownership if required. Litigation – with its delay, expense, and uncertain outcomes – should never be embarked on lightly. As the Court wryly quoted from a previous decision, “a court cannot perform miracles”. It will of course do its best to craft the fairest possible outcome for both parties, but avoiding the dispute altogether is always a better option for everyone involved.

P.S. Don’t forget your cohabitation agreement

As a final thought, if you are living with your life partner, you should have a full cohabitation agreement to cover not only your co-ownership arrangement, but also all the other financial and personal aspects of your relationship that would normally be governed by our marriage laws.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews

“Wouldn’t it be nice to get on with me neighbours?” (from “Lazy Sunday” by Small Faces)

Maintaining friendly relations with the neighbours, or at least an “I’ll ignore you if you ignore me” sort of neutrality, has probably been a primary aim of homeowners since the dawn of history. No doubt even our cave dwelling ancestors were as keen to get on with the Joneses next door as they were to keep up with them. But as we all know, it’s not always easy.

A recent High Court fight over parking rights is unfortunately pretty much par for the course when it comes to neighbourly relations deteriorating into open conflict, both inside and out of the courtroom.

“You can’t park here!” “Yes, we can!”

The setting for this fight: Higgovale, a small and affluent suburb on the slopes of Table Mountain in Cape Town. In one corner: a couple with the right to access their garage using a servitude road. In the other corner: the neighbours, alleged to have impeded the couple’s garage access by parking in the road.

At the heart of the dispute: the road servitude. Servitudes involve a balancing act between the right of the “dominant owner” to exercise the servitude and the right of the “servient owner” to have the servitude exercised in such a way as to impose the “lightest burden” on their property. The tensions inherent in such a relationship can easily escalate into conflict – exactly what happened here.

The garage-owning couple’s initial stance was to ask the Court for a blanket interdict against all parking by the neighbours in the road, but they later softened that to ask only for an order against their garage access being obstructed.

The Court had no hesitation in ordering that the neighbours “are interdicted and restrained from parking vehicles on the servitude area at … Higgovale, in such a manner as to unreasonably obstruct the applicants from entering and exiting their property and exercising their right of way.”

In doing so, the Court took the parties to task for failing to settle their dispute out of court, and urged them “to engage with each other in a manner that promotes the spirit of ubuntu, and the constitutional vision of a caring society based on good neighbourliness and shared concern” (emphasis supplied), and to consider demarcating parking bays in the road as a short-term solution.

The parties now have to pay their own costs (except for the costs of one interim application), and they’re effectively back to square one: having to engage with each other to try to find a fair solution.

What’s a “reasonable neighbour”?

Per the Court (emphasis supplied): “While the common law requires that neighbours act reasonably, the Constitution shows what a reasonable neighbour looks like. She is not only concerned with advancing her own private interests but cares also for the needs of her neighbours. She seeks mutually beneficial solutions. The mindset of the reasonable neighbour is one of collaboration, not competition. She sees herself not as an isolated individual, but a partner in an interdependent community of persons, all of whom are to be respected and valued.”

First prize: Settle!

Courts want us to settle these sorts of disputes in that collaborative spirit, without recourse to law. But if a friendly discussion over a cup of coffee doesn’t resolve the situation, more robust action might be unavoidable – we’re here to help if you need us.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact us for specific and detailed advice.

© LawDotNews