“In life, we never lose friends, we only learn who the true ones are” (Unknown)

Lending money to a friend or family member in need sounds like a natural and informal sort of thing to do. But beware – if relations sour and your friend/relative can’t or won’t repay you, you may not be able to reclaim your money.

The danger is that, if you should have registered as a credit provider in terms of the NCA (National Credit Act) but didn’t, the loan would be an unlawful credit agreement and would therefore be void and unenforceable. You could even face penalties for non-compliance with the requirement to register.

Only “arm’s length” loans fall under the NCA

A recent Supreme Court of Appeal (SCA) case turned on the question of whether or not such a loan was conducted “at arm’s length”.

That’s critical, because only a loan given “at arm’s length” falls under the NCA. The question of what is and isn’t at arm’s length is a complex one, but the factors taken into account by the SCA in reaching its decision provide a good example of what will weigh with a court.

At stake – R15m, loaned informally to a friend on a handshake

- A R15m loan made by one businessman to another was “informal in nature which was sealed with a handshake, with no interest charged.” Later on, the debtor signed an AOD (Acknowledgment of Debt) for the R15m, granting a grace period of six months before interest would accrue on default. The lender had never registered as a credit provider.

- The High Court found both the loan agreement and the AOD were subject to the NCA and therefore unlawful.

- Fortunately for the lender, the SCA overturned this decision on appeal. On the facts, it held that the loan was not “at arm’s length” and therefore not subject to the NCA. Key factors it considered in reaching this decision were –

- The loan agreement was oral and informal,

- The parties had become friends and had “… formed a close bond in personal matters outside the realms of business. The loan was offered as a gesture of friendship”,

- The lender did not normally lend money, and this was a one-time occurrence,

- No interest was levied on the loan except on default and the lender had not “sought to obtain the utmost advantage from the transaction”.

- Bottom line – the lender can breathe a sigh of relief, the loan agreement and AOD are not void in terms of the NCA, and it can pursue the debtor for its R15m.

But – don’t take unnecessary chances!

Concluding an informal loan agreement with a handshake is all very well, but this could well have turned out badly for the lender, and R15m is a lot of money to lose for want of checking for lawfulness upfront.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“…there is no obligation on the [seller] to obtain an occupancy certificate and to furnish it to the [buyers]” (Extract from judgment below)

Imagine this – you buy your dream home, pay for it, take transfer into your name, and move in. But then disaster strikes. The Municipality tells you no occupancy certificate was ever issued for the property and that you must vacate. Now.

Both buyers and sellers should take note of a recent High Court decision highlighting the importance to buyers of getting an occupation certificate from the seller before putting in any offer or insisting on a clause in the sale agreement requiring the seller to produce one before transfer.

What is an occupancy certificate and why is it vital to have one?

It’s confirmation by your local authority that the building complies with the approved building plans and that all other requirements have been met.

Without it, it is unlawful for anyone to occupy the building. You can be ordered to vacate, but that’s not all – other risks include your insurers declining any claims you make, municipal penalties for non-compliance, perhaps threats of a demolition order. You and your family could even be in physical danger if the non-compliance results in electrical hazards, fire risks, structural failure, or the like.

Although the municipality can “grant permission in writing to use the building before the issue of the certificate of occupancy”, that will be a temporary permission only, probably only for a short period and with stringent conditions.

The demolition threat and the court application

- Having bought a property from the owner/builder’s deceased estate, the buyers took transfer and happily moved in.

- To their horror, when a municipal building inspector was called in to inspect the building for defects, it came to light that although building plans had been approved 30 years ago, no occupancy certificate had ever been issued.

- The municipality “suggested” that the buyers vacate immediately and threatened to demolish the building, citing a number of outstanding certificates – completion certificates for the structural and storm water, an electrical compliance certificate, a plumbers’ compliance certificate, a glazing certificate, a gas installation certificate, and a soil poisoning certificate.

- The buyers demanded that the executor of the deceased estate obtain an occupancy certificate for them, and when she refused, they asked the High Court to order her to do so.

- The buyers pointed out that, per a standard clause in their sale agreement, the seller was obliged to give them “vacant possession”. That, they argued, meant “lawful possession” requiring the seller to provide them with an occupancy certificate before transfer.

- The seller (executor) replied that she was not bound by the sale or any other agreement to provide a certificate, that there is no general obligation on a seller to furnish a purchaser of an immovable property with an occupation certificate, that the buyers had been given vacant (“free and undisturbed”) possession, and that anyway the buyers as the new owners should now be the ones to apply for the certificate.

The seller wins, and a warning for buyers

The Court refused to order the seller to provide an occupancy certificate, finding that despite the fact that occupancy of the house was unlawful without the certificate, the buyers had “…clearly received vacant possession. [They] received what they purchased. They had no concerns about what they were purchasing and there is no indication in the papers that they enquired about the occupancy certificate at the time of the sale or prior to taking transfer. They have alternatives available to them … and failed to explain why, as the owner of the property, they have not taken any of the steps available to them.”

In regard to the voetstoots (“sold as is” clause) the Court quoted from a Supreme Court of Appeal decision: “…the absence of the statutory approvals for building alterations, or the other authorisations that render the property compliant with prescribed building standards … does not render the property unfit for the purpose for which it was purchased.”

Perhaps the outcome would be different if a buyer is able to prove that the seller knew of the lack of an occupancy certificate and concealed that, or if a buyer sues for cancellation of the sale agreement or for damages. But that is speculation.

What is clear is this: The occupancy certificate is a vital document and as a buyer you should insist that the seller gives it to you before you make an offer, or that at least a term in the sale agreement obliges the seller to give it to you before transfer.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

24 April 2024 is ‘World Intellectual Property Day’. It’s “an opportunity to explore how intellectual property (IP) encourages and can amplify the innovative and creative solutions that are so crucial to building our common future.” (The UN’s World Intellectual Property Organization)

It’s a case that has been making headlines for years, the “Please Call Me” saga in which Vodacom has been sued by an ex-employee and is now at risk of having to pay over billions of rand to him.

With April being “World Intellectual Property Month”, now’s a perfect time to see what lessons this bitter fight holds for all employers and their employees.

The trainee accountant, his long-distance girlfriend, and his bright idea

- Employed by Vodacom as a trainee accountant, Mr. Kenneth Nkosana Makate was looking for a way to stay in touch with his girlfriend (now wife) with whom he was in a long-distance relationship. As a student she couldn’t afford airtime, a problem faced by many cellphone users at one time or another.

- Long story short, in 2000 Mr. Makate came up with what is now known as the “Please Call Me” (“PCM”) concept – “a brilliant idea: a cellphone user with no airtime could send a request to another user with airtime, to call the former.” He took the idea to his employer, for whom it turned out to be a “resounding success”.

- He asked to be paid for his idea, but Vodacom said it wasn’t obliged to pay him anything. Eventually he sued them on the basis of an agreement, verbally reached between him and Vodacom’s Director of Product Development, to pay him compensation for his idea in the form of a share of revenue.

- Many court battles later the Constitutional Court issued an order declaring that Vodacom was bound by the verbal agreement and ordering the parties to negotiate in good faith to determine an amount of reasonable compensation to be paid.

- More litigation followed, leading most recently to the Supreme Court of Appeal (SCA). Its order setting out how that compensation is to be calculated leaves Vodacom facing a liability reported to total billions of Rand.

- Vodacom is, at date of writing, asking for leave to appeal that order in the Constitutional Court, so the show may not be over quite yet. But regardless of the final outcome, there are valuable lessons to be learned here by all employers (and their employees).

So do your employees own their inventions, or do you?

Generally speaking, our common law rule is that the right to all IP or “intellectual property” (covering patents, designs, copyright, and trademarks – loosely “inventions”), belongs to the employer if the employee created it “in the course and scope of employment”.

But that rule has over the decades led to much uncertainty in cases where employees claim to have come up with their inventions other than in the course of their employment – such as out of working hours, whilst working on their own initiative and on personal matters rather than under the employer’s control and direction, and so on.

For example, one of the many areas of dispute in the Vodacom case was the question of whether or not Mr. Makate, as a junior employee on the accounting side, was acting in the course and scope of his employment when he had his lightbulb moment.

Although, as many commentators have pointed out, that case actually has more to do with being bound by one’s verbal agreements than with questions of intellectual property law, the fact remains that, for employers and employees alike, there is a way to avoid all these potential disputes.

How to avoid uncertainty and dispute

The answer of course is to set out clearly in all contracts of employment and related policy documents who will own such inventions. A standard clause to protect employers in this regard might provide that any IP created by the employee during the period of employment are presumed to belong to the employer, no matter the circumstances in which it is created.

Such a clause should ideally be customized to reflect the nature of the employer’s business and the employee’s job description, it should ensure fairness and practicability, it should comply with legislative limitations applying to various types of IP, and it should lay out incentives and procedures for employees to come up with bright ideas and share them.

Every situation will be unique, so specific professional advice tailored to meet your business and its particular needs is essential.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“It’s important to remember your competitor is only one mouse click away” (Doug Warner)

Your website, social media profiles, and other online platforms play a vital role in your business strategy and in staying ahead of your competition at all times.

However, it’s not just about marketing effectively. Ensuring compliance with regulations is equally crucial, although often overlooked.

Why is Compliance Important?

Compliance ensures that your business:

- Meets all legal requirements.

- Reduces risks associated with user engagement.

- Enhances your brand’s image.

- Builds trust and loyalty with users.

- Safeguards your reputation.

- Prevents unnecessary costs.

A Checklist for Website Compliance

Website compliance involves adhering to various laws, regulations, and standards governing online operations and content. Here’s what it entails:

- Legal Compliance: Your website must follow local, national, and international laws, covering online business, intellectual property, and consumer protection requirements.

- Accessibility Compliance: Websites should be accessible to people with disabilities, as mandated by some countries’ laws.

- Cookie Compliance: Inform users about cookies and obtain their consent before placing them on their devices, as required by many countries.

- Privacy Compliance: Comply with privacy regulations when collecting user data, such as POPIA in South Africa and (where applicable) GDPR in the EU.

- Security Compliance: Implement security measures like encryption and secure logins to protect user data and prevent unauthorized access.

- Content Compliance: Ensure content doesn’t violate copyright or trademark laws.

- Financial Compliance: Adhere to regulations for online payments and financial transactions if your website conducts such activities.

- Advertising Compliance: Ensure ads meet advertising standards and regulations to avoid deception or violation of laws.

- Terms of Service/Supply and Policies: Make legal documents clear, transparent, and legally sound for users to agree to.

- Industry-Specific Compliance: Some industries have specific regulations, like healthcare websites complying with health information privacy laws.

Integrate compliance into step 1 of your website’s development

Integrate compliance into the very earliest developmental stage of your website, focusing not only on content but also design and process. This ensures that your online presence remains compliant from the outset, reducing the risk of non-compliance issues down the line.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“The first thing we do is, let’s kill all the lawyers.” (Shakespeare)

Shakespeare must have had an unhappy experience or two with the lawyers of his time to have one of his characters utter that threat, but the reality is that every aspect of our lives is touched at one time or another by the law and the only way to navigate legal waters confidently and safely is with professional guidance.

While many people may feel intimidated by the legal system, seeking legal advice can help to avoid costly mistakes and to ensure that your rights are protected. Here’s a brief guide on when and why you should seek legal help.

When should you seek legal help?

The short answer of course is “any time you are faced with a significant legal issue”, but let’s list some of the more common and important scenarios in which specific legal advice and assistance sometimes seems overkill, but is actually a no-brainer –

- Buying or selling a property: The process of buying or selling a house involves several legal requirements, from contracts and the transfer process to the financial preparations. Asking us for legal advice before you sign anything can help to ensure that the transaction is legally binding and protects your interests.

- Starting a business: Setting up a business requires a good understanding of all the legal aspects. We can advise on the best legal structure for your business, help draft contracts and agreements, and ensure that your business complies with all relevant laws.

- Drafting a will: A valid will is an absolutely vital document to ensure that your loved ones are properly provided for when you die. We will help you draft a will that clearly expresses your wishes and protects the interests of your beneficiaries.

- Getting married: Choosing the correct “marital regime” before you marry is essential and we will help you to make the best choice and to structure the right ANC (ante-nuptial contract) to protect you both.

- Getting divorced: The long-term personal and financial ramifications of divorcing make legal assistance indispensable. The earlier you approach us for advice and help, the more effectively we can help you navigate this unhappy process with as little delay and dispute as possible.

- Employer/employee contracts and disputes: Our employment and labour laws are complex and the consequences of getting them wrong can be extremely serious. There is no substitute for upfront and specific legal advice on structuring employment contracts and handling disputes as they arise.

- Dealing with disputes: Whether it’s a dispute with an employer, an employee, a neighbor, a customer, or indeed anyone else, seeking legal advice can help you resolve the issue and protect your rights. We can help you understand your rights, stay on the right side of the law, negotiate a settlement, seek arbitration, or if need be, represent you in court.

- Any brush with our criminal laws: Being accused of a crime can happen to anyone at any time. Perhaps you are arrested after failing a breathalyser test or threatened with a statutory offence relating to your tax affairs. Perhaps it is something even more serious or perhaps it seems inconsequential, but don’t take any chances here – ask us for help immediately or you could end up with a criminal record and serous penalties.

What about small claims, minor disputes, and the like?

You probably won’t need to incur the costs of formal legal advice and help when smaller and less important disputes and issues arise, but it’s always wisest to check with us first. Something seemingly minor could risk serious consequences down the line if not properly handled, and we’ll tell you whether or not that is the case.

Beware false economy

Legal assistance can be costly but beware the temptation to penny-pinch. Our law reports are full of cases where, for want of a little upfront and specific legal advice, litigants end up fighting – and often losing – long, bitter, and costly cases through court after court.

“A stitch in time saves nine” goes the old adage – wise advice indeed, and well worth heeding.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“The conditional acceptance of an offer amounts to rejection of same and not the conclusion of a contract, but may be a counter–offer.” (Extract from judgment below)

A good offer comes in for your property, so you accept it. But you’re not happy with a few of the terms, so before you sign you make a few changes to the offer. Maybe they are big changes, maybe they seem inconsequential.

Either way, you are now effectively negotiating, not accepting the offer. You have in fact just rejected it. Unless the buyer now accepts your amendments in writing (by initialing or counter-signing against your alterations), you almost certainly have no valid sale.

Thinking that you have a valid sale when you don’t is a common and easily-made mistake, and a recent High Court decision shows just how important it is for both seller and buyer to be aware of this danger.

The property auction, the counter-offer, and the commission claim

- A property on auction attracted a top bid of R1.85m and after some haggling the buyer put in a second offer of R1.9m.

- The seller accepted this second offer, but critically with amendments. The parties could not agree on these outstanding issues, with the result that the seller sold the property to another buyer without the auctioneers’ involvement.

- At which stage the auctioneers sued the seller for commission, arguing that a sale had been concluded at R1.9m because the amendments to that offer were “not material” ones (in other words, they weren’t important, significant or essential terms). The terms in question related to who was to receive the agreed occupational interest and to the issue of a gas compliance certificate. Neither amendment, argued the auctioneers, was material to the sale.

- The Court however disagreed, commenting that “In principle, anything more or less than an unqualified acceptance of the entire offer amounts to a counter-offer and constitutes a rejection of the original offer.” It accordingly dismissed the auctioneer’s claim for commission on the basis that the seller’s amendments were material and amounted to a counter-offer which the buyer had never accepted. In other words, no sale agreement had ever come into existence.

So, do you have a binding sale agreement?

If the amendments to the offer have been accepted and signed by both buyer and seller, no problem – the counter-offer has been accepted and you have a binding sale agreement.

Otherwise, as our courts have put it: “When parties conclude an agreement while there are outstanding issues requiring further negotiation, two possibilities would follow: no contract formed because the acceptance was conditional upon consensus, or a contract formed with an understanding that the outstanding issues would be negotiated at a later stage.” Deciding which is which means trying to deduce the parties’ intentions from their conduct and other circumstances – a grey and specialist area requiring specific legal advice.

Bottom line

Making a counter-offer can be an excellent tactic for negotiating towards agreement, but be very careful with the concept of “conditional acceptance”. It is actually not an acceptance at all but a rejection of the offer and could well be a counter-offer requiring acceptance by the other party in order for there to be a valid sale. Avoid all doubt by making sure everything is signed and counter-signed.

As always, ask us before you sign anything!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“…the prospect of continued employment must be shown to have been objectively intolerable and the employee must have resigned due to the intolerable situation and not for another reason.” (Extract from judgment below)

Perhaps you are an employer, and that troublesome employee who you’ve been hoping would resign does exactly that. Saving you, as you see it, from the risk, hassle, and expense of disciplinary or retrenchment proceedings. But are you really home and dry?

Or perhaps you are an employee, driven to resign by your employer’s constant maneuvering to make your continued employment unbearable. Do you have any recourse?

The answer to both questions lies in the Labour Relations Act’s definition of “dismissal”, which includes an employee resignation when “an employee terminated employment with or without notice because the employer made continued employment intolerable for the employee.”

And when there’s a dismissal, it has to be a fair one or the employer is in for a very expensive lesson. As we shall see …

The three requirements for “constructive dismissal”?

As confirmed in the Labour Court judgment we discuss below, there are three requirements for constructive dismissal to be established, all three of which must be proved by the employee –

- The employee must have terminated the contract of employment, and

- The reason for termination of the contract must be that continued employment has become intolerable for the employee, and

- It must have been the employee’s employer who had made continued employment intolerable.

Note that there is no constructive dismissal if an employee resigns for any other reason, for example “because he cannot stand working in a particular workplace or for a certain company and that is not due to any conduct on the part of the employer.”

And a test for “intolerability”

“Intolerability”, said the Court, “is a high threshold, far more than just a difficult, unpleasant or stressful working environment or employment conditions, or for that matter an obnoxious, rude and uncompromising superior who may treat employees badly. Put otherwise, intolerability entails an unendurable or agonising circumstance marked by the conduct of the employer that must have brought the employee’s tolerance to a breaking point.”

The case of the specialist fraud and risk investigator in a bullet proof vest

- A specialist fraud and risk investigator resigned from his employment with a bank after 17 years’ service, then successfully referred an unfair dismissal dispute to the CCMA (Commission for Conciliation, Mediation and Arbitration), claiming constructive dismissal.

- Suffering health problems and involved in high-risk investigatory work which put his physical security at risk (hence no doubt his wearing a bullet-proof vest), he claimed to have been subjected to ongoing victimisation, bullying and harassment. His complaints included grievance disputes not being attended to, refusal of compassionate leave, poor work performance assessments, disciplinary and incapacity proceedings – the list goes on.

- Finding on the facts that there was “an accretion of conduct creating an increasingly oppressive work relationship for [the employee], with no functioning mechanism available to halt the deterioration”, the Court held that the employer had made the employment relationship intolerable. The employee was entitled to regard his resignation as a constructive dismissal and, that dismissal being an unfair one, the Court confirmed the CCMA’s compensation award of ten months’ remuneration.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“MTl’s business clearly amounted to an unlawful ponzi-scheme, i.e. a fraudulent investing scam promising high rates of return to investors and generating returns for earlier investors with investments taken from later investors.” (Extract from the MTI judgment)

Recent media reports of the MTI (Mirror Trading International) liquidators making repayment demands of investors highlight once again the dangers of falling for “too good to be true” investment schemes.

The problem is that by their very nature, all pyramid schemes (including “ponzi” schemes) eventually fail, leaving the vast majority of investors with nothing but the hope of being awarded a partial dividend on their claims when the holding entity is eventually liquidated.

But what if an investor is one of the “lucky early birds” who got paid out before the scheme’s collapse?

Debunking the “early bird investor catches the worm” myth

A common myth is that the only losers in a collapsed pyramid scheme are those investors who didn’t get their money out in time, and that the “early birds” who did act quickly are winners in the equation.

The problem for them is that liquidators have wide powers to reclaim payouts made to investors (as creditors) before liquidation. The idea is that payouts by definition come from new money paid in by new investors, and that to be fair to them it is necessary to put everything back into the pot for all investors and other creditors to share according to their claims. But of course they only share in what’s left after all the liquidation costs and fees have been settled, and in a large and complex liquidation like MTI’s those costs will be particularly substantial.

The practical issue is that whatever was paid out to investors/creditors – both by way of the original investment and the “profit” on it – is likely to be claimed back by the liquidator. And the investor forced to repay everything is left with nothing but a concurrent claim in the liquidation.

Of course a liquidator’s prospects of recovery will be boosted if they can obtain a court declaration of unlawfulness of the scheme and invalidity of the investment contracts (as has already happened in the MTI liquidation), but let’s see how that could then play out in practice.

The liquidator’s options for recovery

To summarise the options available to a liquidator in recovering payouts made before liquidation –

- “Voidable preference”: If the payout was made within six months prior to liquidation and immediately thereafter the company’s liabilities exceeded its assets, it is repayable to the liquidator unless the investor can prove that that the disposition was made “in the ordinary course of business” and without intention to prefer one creditor above another. That could be hard to prove in the case of a pyramid scheme.

- “Undue preference”: If at any time a payout was made by the company with the intention of preferring one creditor above another, it is repayable to the liquidator if the company’s liabilities exceeded its assets at that stage. In this case, the onus is on the liquidator to prove the intention to prefer, but that may perhaps be easier to prove in a pyramid scheme scenario than in other corporate failure scenarios.

- “Disposition without value”: Monies paid out to a creditor at any time must be repaid to the liquidator if the company received no “value” in return, subject to –

- Where the payout was made more than two years prior to liquidation, the liquidator must prove that immediately thereafter the company’s liabilities exceeded its assets.

- But if the payout was made within those two years, the onus switches to the creditor to prove that immediately thereafter the company’s assets exceeded its liabilities. In the case of a pyramid scheme that may be impossible to prove.

Note that the creditor in such a case will also generally lose their claim against the company.

- “Collusive dealing”: If the liquidator can prove that a creditor colluded with the company to pay out monies with the effect of prejudicing creditors or of preferring one creditor above another, the colluder will not only forfeit their claim but can also be ordered to pay in a penalty of up to the same amount. A liquidator could for example try to prove that the investor/creditor was aware of the unlawfulness of the scheme at the time of the payout.

Even worse, could investors lose a lot more than they put in?

Media reports suggest that an MTI investor, who invested R20,000 and was paid out R21,000 shortly before liquidation, received a demand from the liquidators to repay not just his initial investment and profit, but for 600% of what he put in. The sum claimed (at date of writing) is R122,000, that being the current value of the bitcoin he initially invested – the argument being presumably that what was disposed of was “property” (bitcoin), in which case the liquidators would be entitled to reclaim either the bitcoin or its value at the date the disposition is set aside. The justification will no doubt be that that is what the company and its creditors as a whole have actually lost as a result of the disposition. If our courts agree with that view, being sued for a great deal more than the original investment will be a particular risk when the investment is a volatile asset like bitcoin.

The High Court has previously declared MTI an illegal and unlawful scheme and all agreements between it and investors unlawful and void, but that of course is only the first step for the liquidators in proving their claims against investors. Media reports suggest that many investors are lawyering up to oppose the claims so we must wait and see how it all plays out in the courts.

Regardless, the risk of not only losing the original investment but then also having to cough up a great deal more over and above that certainly does fire yet another warning shot across the bows of anyone tempted to invest in any scheme promising unrealistic returns. Prospective investors shouldn’t part with a cent until they confirm that the scheme is actually legitimate.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

The National Minimum Wage (NMW) for each “ordinary hour worked” has been increased from 1 March 2024 by 8.5% from R25-42 to R27-58.

Domestic Workers: Assuming a work month of 21 days x 8 hours per day, R27-58 per hour equates to R220-64 per day or R4,633-44 per month. The Living Wage calculator will help you check whether or not you are actually paying your domestic worker enough to cover a household’s “minimal need” (adjust the “Assumptions” in the calculator to ensure that the figures used are up to date).

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

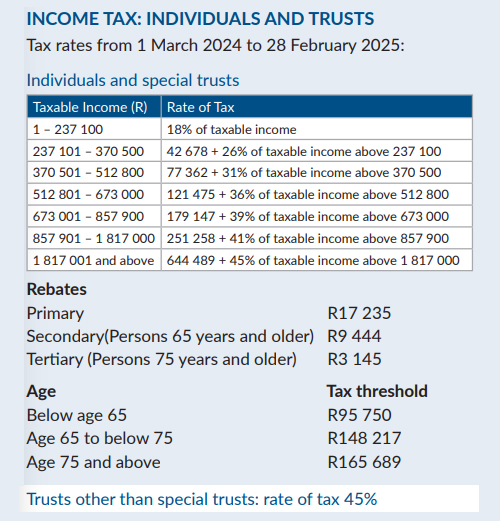

The unchanged transfer duty and tax tables, with a note on fiscal drag

Unchanged from last year, so taxpayers can breathe a sigh of relief that rates have not been increased as many forecasters had feared.

But the other side of the coin of course is that there is no inflation adjustment to the rates this year, which means that “fiscal drag” will leave you paying more tax if your inflation-linked increase pushes you into a higher tax bracket. Effectively, the buying power of your net income will fall. Plus if your property has increased in value into a higher threshold, your buyer will pay more transfer duty.

![]()

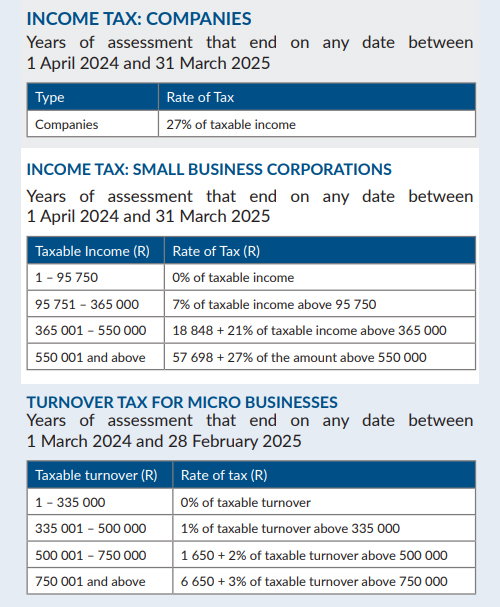

Source: SARS

Source: SARS

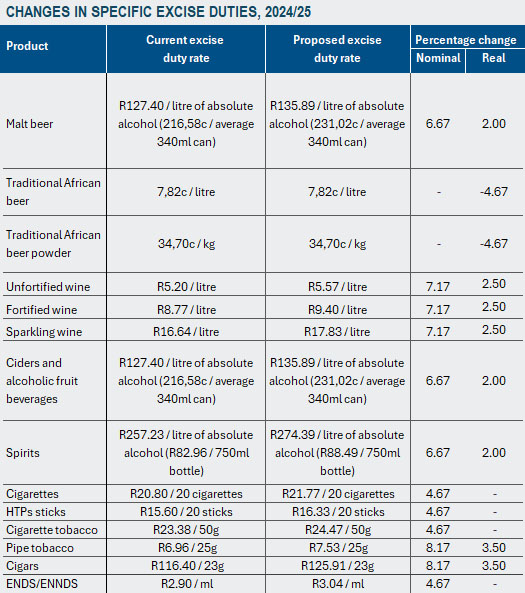

“Sin taxes” up – the details

Source: National Treasury

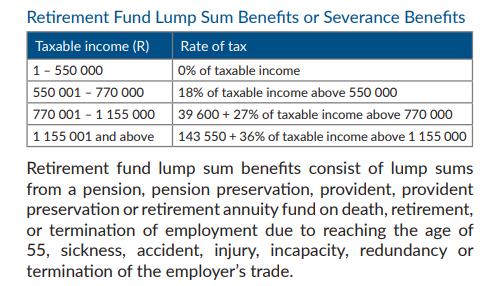

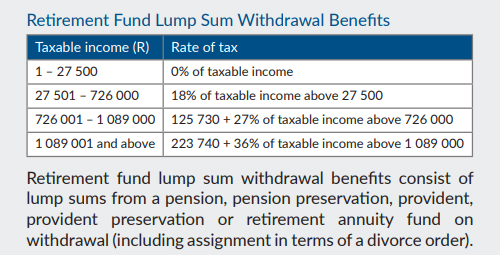

Retirement funding and the “two-pot” reform proposal

Source: SARS

Source: SARS

The proposed “two-pot” retirement reform: Per National Treasury: “Early access to retirement funds – “The two-pot retirement system will allow retirement fund members to make withdrawals from their retirement funds while they are still active members, so members need not resign to access part of their retirement benefits. … This reform is proposed to come into effect on 1 September 2024. The National Treasury aims to finalise the legislative process rapidly in the next few months to ensure that industry and regulators can prepare for implementation. Policy research and engagement continues on the outstanding auto-enrolment, mandatory enrolment and consolidation retirement reforms.”

The proposals and their tax implications are complex and subject to change, but currently provide for a one-off withdrawal of up to R30,000 on implementation, and thereafter annual “savings withdrawal benefits”.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews