“We have this handy fusion reactor in the sky called the sun; you don’t have to do anything, it just works. It shows up every day” (Elon Musk)

Eskom’s no-end-in-sight loadshedding, rising electricity costs, South Africa’s abundance of sunshine, and the global move to sustainable energy solutions have all contributed to the current boom in home solar photovoltaic (PV) roof installations.

They don’t come cheap, but quite apart from the direct practical and financial benefits of going as much off-grid as possible, you will be boosting your property’s resale value (supposedly by between 4% and 8% depending on the system you install and your current house value). And at least one municipality is already planning to pay you for any excess power you feed back into its grid – expect that to become a growing trend.

Moreover, in addition to the existing tax incentives for businesses installing solar, the Budget Speech has promised both an expansion of the tax incentives and the introduction of a new tax incentive for individuals in the form of a 25% tax rebate (maximum R15,000 per individual) of the cost of “new and unused” solar panels (not inverters or batteries) – available for 1 year only (1 March 2023 to 29 February 2024) “to encourage investment as soon as possible”.

Step 1: How to choose an installer for a safe and legal installation

Before you accept a quote for your solar project (typically some solar panels, an inverter and a battery or two), there are several regulatory requirements to bear in mind, and the best way to ensure that you comply with everything (quite apart from the safety aspect) is to choose an installer with a good track record and the right qualifications. Bear in mind that you will need your installer to issue a valid compliance certificate for the system for several reasons –

- To complete the process of getting the system authorised (see below),

- To add the system to your homeowner’s insurance,

- To ensure that the system’s warranties aren’t voided, and

- To allow you to claim the new tax rebate as above.

Questions to ask a prospective installer: Here’s a list of questions to ask (adapted from the excellent list in “City of Cape Town’s Checklist for safely going solar” on cape{town}etc) –

- What prior experience do you have in solar PV installations?

- What three recent clients of yours can I phone for references?

- Did you design, supply and install the systems, or did you only carry out one or two of these steps?

- Are you an accredited service provider under PV Green Card, SAPVIA or P4 Platform?

- Can you supply proof of electrical Certificates of Compliance and/or professional engineer sign-offs on previous installations?

- Can you prove that your previous installations were correctly authorised by the local authority (or Eskom if direct customers)?

- Do you employ or subcontract qualified staff to design and install systems? (Note: The City of Cape Town suggests you ask for “proof of up-to-date registration (a wireman’s licence and DoLE registration)”).

- Is the inverter you are quoting for on the local authority’s approved inverter list? (Note: Find the City of Cape Town’s list here; if you are told that your local authority has no such list, get written confirmation).

- If you propose a “grid-tied system” (see definition below) do you have available an Engineering Council of South Africa (ECSA) registered professional to sign it off?

- Are the solar PV panels in compliance with SANS/IEC standards? (Note: The City of Cape Town article recommends you get a certificate of compliance for SANS/IEC 61215:2015 / SANS/IEC 61646:2016).

- Are you registered with SAPVIA and the ECB? (Note: Per The City of Cape Town “it’s not compulsory but shows commitment to industry best practice.”)

- What warranties apply to your installation and the components? (Keep proof, with all manuals).

- Is your quote comprehensive and does it include installation of circuit breakers (specialized to the DC current from the panels), obtaining SSEG registration (see below) and a Certificate of Compliance?

Step 2: How to comply with all regulatory requirements

- Next, comply with the SSEG (Small Scale Embedded Generation) process – have your chosen installer do everything on your behalf. You will need to register the system for authorisation with either Eskom or your local municipality (whichever supplies your electricity).

- Note that authorisation is needed whether or not your system will be feeding electricity back into the grid. If your system will connect to the grid (via your distribution board or directly) it will be a “grid-tied” one – either “feed-in” or “non-feed-in” depending on whether or not it will export excess power to the grid. If it’s “non-feed-in” you will need to have “Reverse Power Flow Blocking” installed to prevent any excess electricity feeding back into the grid. If it’s a “feed-in” you have more hoops to jump through as an Electricity Supplier. To complicate matters further, you also get “hybrid” systems which can be either on-grid or off-grid. For more detail read the City of Cape Town article referenced above (“The three types of systems” section).

Incidentally none of this is just bureaucratic red tape – suppliers need to know when it is safe for their technicians to work on the grid, there are issues related to grid management, and there are home safety issues around risk of fires and other hazards.

Check with your supplier (local authority or Eskom) whether you need any authority for a standalone (“off-grid”) system. At date of writing, at least one municipality – City of Cape Town – does require registration “to ensure they are not mistaken for grid-tied systems”.

- The process itself, let alone the terminology and technical requirements (such as wiring diagrams and an engineering sign-off), is complicated. Have your installers do everything for you, and in doubt contact your municipality’s electricity department (or Eskom direct if applicable) for more information.

- Failing to register and obtain written authorisation prior to installation could be an expensive business, with some municipalities threatening to use aerial photos, inspections and billing analysis to locate unauthorised systems, which will then attract penalties, contravention notices, and supply disconnection. Failure to register might even cause your insurers to reject a claim and that could be disastrous – think for example of a system failure causing a house fire.

- If you live in a “community scheme” like a sectional title complex or a homeowner’s association complex, check your Rules and Regulations and get necessary consents upfront.

- Make sure that all aspects of the installation comply with local regulations to reduce the risk of any future insurance claims being rejected for non-compliance. For example, check the technical requirements for roof structures (ensure that they can cope with the weight and wind load of panels), also you may or may not need building plans, plus some municipalities have lists of approved inverter makes and models.

Talking of which, don’t forget to send the compliance certificate to your insurers with an instruction to add your new system to your homeowner’s policy.

Safety and recourse for poor work

The City of Cape Town checklist referenced above is well worth a full read regardless of where you live – read in particular the sections on safety and “Recourse for poor work”.

A final thought – should you ditch Eskom altogether?

A final thought – you could of course go off-grid entirely. It’s tempting isn’t it to wave Eskom and all its issues a cheerful good-bye, you’ll be avoiding a lot of the paperwork mentioned above, plus you won’t be paying Eskom’s “fixed service connection fees” any longer. But then you really will be on your own, with no connection whatsoever to your municipal or Eskom supply. Think about the effect on your resale value as well as the short-term pros and cons of making that sort of decision!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

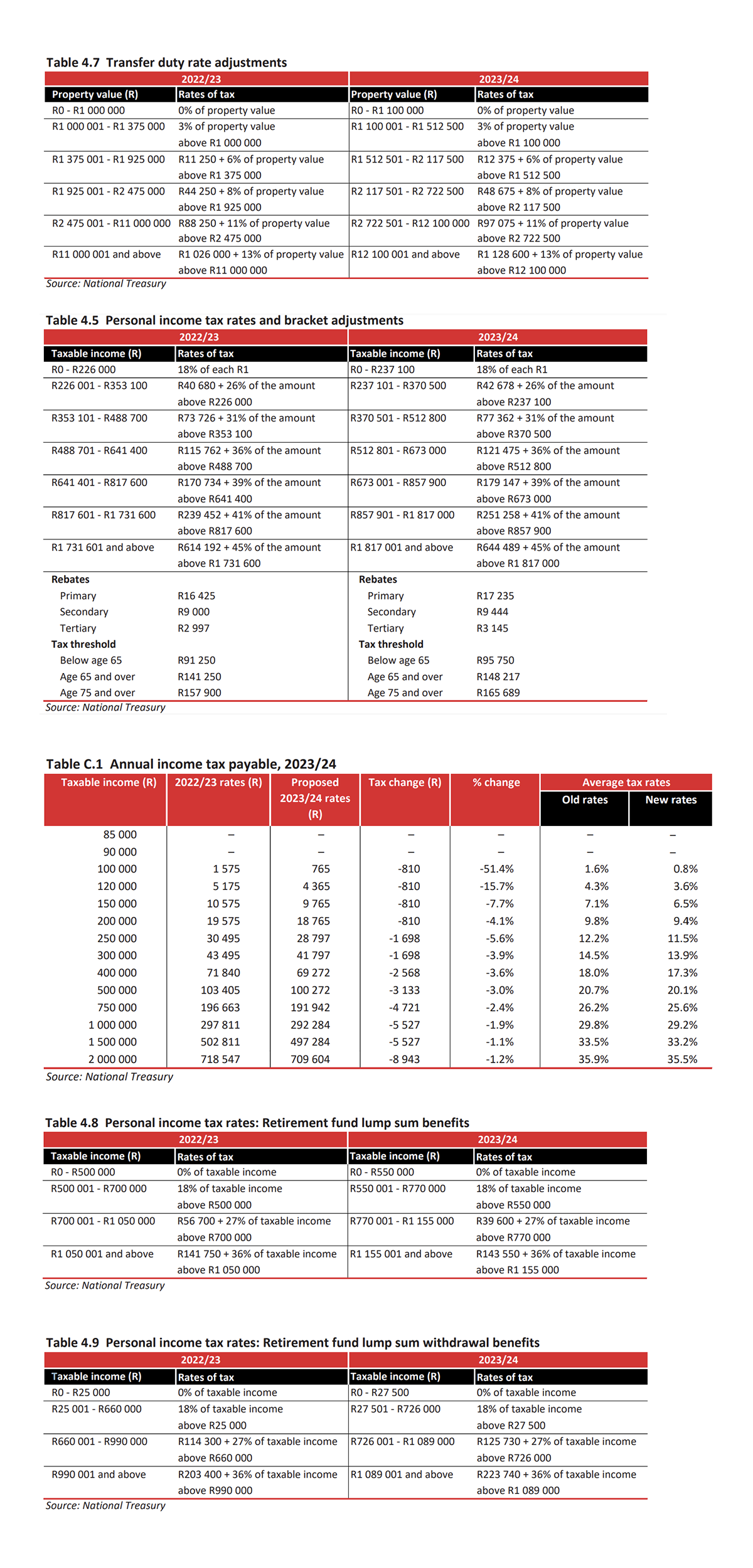

How much will you be paying in income tax, petrol and sin taxes? Use Fin 24’s four-step Budget Calculator here to find out.

Have a look at the tax tables below for the new tax rates and comparisons with last year’s rates –

“The American Automobile Association estimated in the five years prior to 2016 that 16 million drivers in the United States have suffered damage from potholes to their vehicle including tire punctures, bent wheels, and damaged suspensions with a cost of $3 billion a year.” (Wikipedia)

Pothole problems are by no means exclusive to South Africa, but we certainly do seem to have more than our fair share of them.

As a recent High Court decision illustrates, if you suffer any form of loss as a result of a pothole, hold whoever is responsible to account. Sue for your damages!

Injured motorcyclist awarded damages

- Descending a pass on a provincial road with a group of fellow bikers, a motorcyclist leaned into a corner on a sharp bend then hit and went over a pothole. He lost control of the bike which then skidded across the road surface, injuring his shoulder and arm and damaging his clothing and motorbike.

- He was taken by ambulance to hospital, underwent surgery, and although discharged after four days, still two years later is taking painkillers and undergoing physiotherapy for ongoing pain and restricted use of his shoulder and arm.

- An expert confirmed that he had had no opportunity to avoid the pothole and thus the accident. It was also clear that an attempt had been made to repair the pothole.

- He had suffered permanent injuries which “have left him greatly compromised and vulnerable.”

- He sued the Province for damages, and was no doubt pleasantly surprised when the MEC made no effort to defend the action. However, he still had to prove his claim…

Proving negligence, and loss

The Court confirmed that the onus is on a claimant to prove negligence on the part of the local authority, even when, as in this case, the MEC had taken no steps to defend the claim and it was uncontested.

Finding from the uncontradicted evidence of the biker and his expert witnesses that the MEC was solely negligent for the accident in failing to live up to the responsibility “of building, maintaining road infrastructure and putting up road signs cautioning road users of the dangers of potholes”, the Court held him liable for the claimant’s proved damages.

The Court awarded the claimant damages of R850,000 in respect only of those aspects of his claim that he had led evidence to support (future medical treatment and general damages). That figure could increase – although he had failed to produce evidence in support of his further claims (for loss of earnings and damage to property), he can still re-institute action for them.

So, do you have a claim?

You quite possibly do have a claim for any losses you suffer after hitting a pothole. Considering our courts’ attitude to the responsibility of local authorities for road maintenance, proving negligence may not be that hard. Line up also evidence to support all aspects of your claim.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

Employers and employees need to keep an eye on the annual increases in both the National Minimum Wage and the Earnings Threshold, summarised below for your convenience. Both are effective from 1 March 2023.

The National Minimum Wage increase

The National Minimum Wage (NMW) for each “ordinary hour worked” has been increased by 9.6% from R23-19 to R25-42. Workers who have concluded learnership agreements in terms of the Skills Development Act are entitled to a sliding scale of allowances.

Domestic workers

Domestic workers were brought into line with the NMW in 2022, and assuming a work month of 21 days x 8 hours per day, R25-42 per hour equates to R4,270-56 per month. The Living Wage calculator will help you check whether or not you are actually paying your domestic worker enough to cover a household’s “minimal need” (adjust the “Assumptions” in the calculator to ensure that the figures used are up to date).

The Earnings Threshold Increase

The annual earnings threshold above which employees lose some of the protections of the Basic Conditions of Employment Act has been increased by 7.6% from R224,080-48 p.a. (R18,673-87 p.m.) to R241,110-59 p.a. (R20,092-55 p.m.).

“Earnings” (for this purpose only) means “the regular annual remuneration before deductions, i.e. income tax, pension, medical and similar payments but excluding similar payments (contributions) made by the employer in respect of the employee: Provided that subsistence and transport allowances received, achievement awards and payments for overtime worked shall not be regarded as remuneration”.

Some employees enjoy only limited BCEA protection even if they earn below the threshold – notably any “senior managerial employee” (“an employee who has the authority to hire, discipline and dismiss employees and to represent the employer internally and externally”), any “sales staff who travel to the premises of customers and who regulate their own hours of work” and any “employees who work less than 24 hours a month for an employer”. Take specific advice for details.

The threshold also impacts on some of the protections provided in the Labour Relations Act –

- Employees earning less than the threshold, if contracted to a client for more than three months through a temporary employment service (“labour broker”) are deemed to be employed by the client unless they are actually performing a temporary service.

- Fixed-term employees earning below the threshold are deemed to be employed indefinitely after three months unless the employer has a justifiable reason for fixing the term of the contract.

Turning to the Employment Equity Act, employees earning over the threshold can only refer unfair discrimination disputes (other than disputes based on sexual harassment) to the Commission for Conciliation, Mediation and Arbitration (CCMA) with the consent of all parties. Otherwise, they must go to the Labour Court for arbitration.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“The approval of building plans is not a mere formality in town planning and compliance with building standards promote public safety … The courts should not permit landowners to erect illegal structures on their land and then present the authorities with a fait accompli created by their illegal actions” (Extracts from judgment below)

What do you do if your neighbour starts building next door without municipal plans? A recent High Court decision confirms your right to apply for demolition.

The pensioner who built an apartment block illegally

- A property owner decided to build a multi-story block of eight apartments on his land. According to media reports he is a pensioner who spent his R900,000 pension payout on the project and planned to live off the resultant rentals of some R40,000 p.m.

- The building, which he had told his neighbours was just going to be a garden cottage, was illegal on four counts –

- No building plans were approved by the local Council,

- The structure encroached on building line restrictions imposed in the Town Planning Scheme,

- The structure did not comply with the zoning of the property,

- A restrictive condition in the title deed was contravened in that the title deed permitted only one dwelling on the property and the owner was erecting a second.

- The owner failed to comply with two “stop building” orders from the Council. Then he undertook to cease the works but instead accelerated them.

- Two of his neighbours urgently applied to the High Court to interdict further building, and the Court ordered the owner to demolish the building.

- The owner appealed this order to a “full bench” of the High Court asking for the demolition order to be postponed whilst his application to the Council for rezoning and removal of the restrictive conditions was finalised.

- Although the Council had approved the rezoning of the property it had specifically noted that it did not condone the partly constructed building, which was illegal because no building plans had been approved and the building encroached on the building lines.

- The neighbours, held the Court, had standing to apply for a demolition order, in that although their land had not been encroached upon, their rights had.

- In deciding to exercise its discretion in favour of demolition, the Court noted that the neighbours had taken steps to protect their rights immediately it became apparent that the owner was not constructing a garden cottage but an apartment block. They reported the illegal structure to the Council, and it weighed heavily with the Court that the owner carried on building even when he knew it was an illegal structure.

- The owner must demolish the building.

Bottom line – if your neighbour starts building illegally, take immediate action!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“Oh, what a tangled web we weave when first we practice to deceive” (Sir Walter Scott, quoted in the judgment below)

It’s a sad fact of life in today’s business world that as an employer you must remain constantly on guard against the dangers of “CV fraud”.

First prize of course must always be prevention – verify all claimed qualifications and work experience, accept nothing on trust. But if you do get caught out, our courts will help you if they can, as witnessed by a recent High Court case.

The “graduate” who forged a B.Sc degree

- An employee was found to have been employed, and to have been accepted into his employer’s graduate development programme, on the basis of forged qualifications in the form of a forged B.Sc degree (in Chemical Engineering) and a falsified academic record.

- His fraud was only discovered after some 8 years, and when he resigned (after disciplinary proceedings against him began) his employer reclaimed the +R2.2m it had paid him over the years.

- The employee objected, claiming that he had provided value to his employer in his work. The Court was unimpressed, no doubt at least in part because of the employer’s evidence that, as it was a bulk supplier of water to millions of people, having an unqualified person working for it (performing calculations on the type and quantity of chemicals to be added to the water) “could potentially have incredibly serious consequences for the general populace.”

“Fraud unravels everything” – goodbye R2.2m and a pension fund

Held the Court (quoting from a well-known English case on fraud): “No court in this land will allow a person to keep an advantage which he has obtained by fraud. No judgment of a court, no order of a Minister, can be allowed to stand if it has been obtained by fraud. Fraud unravels everything.” (Emphasis added)

The employee, said the Court, “set out to deceive and wove his web accordingly. He achieved his goal. He has now become entangled in a web that he alone devised and cannot now be heard to complain of the consequences that must follow.”

Not only must he now repay every cent of the R2,203,565.04 he earned through his fraud, plus interest, but his pension benefits (which are normally secure from creditor claims) can be used for the purpose. To rub a final dose of salt into his wounds, he must also pay legal costs on the punitive attorney and client scale – no doubt the Court’s findings as to his untruthfulness as a witness contributing to that result.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“In my view, given the difficulties of a sheriff or his deputy accessing a security complex in the absence of the occupant for the purposes of service in terms of rule 4, service of process by way of it being handed to the security guard at the complex, a responsible employee older than 16 years, is valid and effective service on the debtor.” (Extract from judgment below)

Moving house (or office) will mean a busy time and a long “to do” list.

Here’s an action item to add to the “Priority” section of your list: Give notice, in the required format, to everyone you have contracted with. Otherwise you could well, like the debtor in this case, wake up one morning to find your bank account frozen. Or the Sheriff of the High Court knocking on your door with a Warrant of Execution against your property.

Why is your “domicilium citandi et executandi” so important?

A “domicilium citandi et executandi” (“domicilium” for short), is a bit of Latin wording you will see in many agreements, and in simple terms it’s the address you nominate in a contract where legal notices may be sent to and legal process (such as a summons) served on you.

As we shall see below, it’s vital to take it seriously, both when you initially choose an address in the contract, and if/when you later move.

Debtor’s bank account frozen after summons served on a complex security guard

- An occupant in a security complex with “many” residents bought a motor vehicle on instalment sale agreement, specifying his residential address as his domicilium.

- Eventually after he surrendered the motor vehicle it was sold on auction and he was notified to pay the balance of R108k plus interest.

- When he moved to another security complex, he phoned the creditor to advise his new address. Critically however, he didn’t follow that up with a formal advice of change of domicilum in the required format.

- When the creditor issued Summons, the Sheriff tried first to serve it at the new address but failed when that complex’s security guard said the debtor was not yet living in the unit, although his possessions were there.

- The Sheriff then served the Summons at the old address (the debtor’s chosen domicilium), by handing it to the complex’s security guard.

- Unsurprisingly there was no notice of intention to defend from the debtor, whereupon the creditor took a default judgment and attached and froze the debtor’s bank account (leaving him, so he said, unable to pay his covid-related hospital and medical expenses).

- The debtor asked the High Court to set aside (“rescind”) the judgment, arguing amongst other things that the summons hadn’t been properly served on him.

Why the debtor lost

- As the Court put it: “Service on an address chosen by a debtor as the domicilium citandi et executandi constitutes good service even if the debtor is known not to be residing at the domicilium address, is overseas or has abandoned the premises.” In other words the summons is considered properly served whether you are still at the address or not.

- “The manner of service at a domicilium address, however, must be effective. It must be such that the process served at the domicilium citandi et executandi would, in the ordinary course, come to the attention of and be received by the intended recipient.”One way of meeting that requirement is to serve the process on a “responsible employee” – and, held the Court, security complexes not being easy to access in the absence of an occupant, it made no difference that the security guard in question worked not for the debtor but for the complex.

- The obligation is on a debtor changing address “to update or amend the debtor’s chosen domicilium address with the credit provider.” You have only yourself to blame for the consequences if you forget to do that.

- Critically, you must advise a change of domicilium in whatever manner the contract requires (usually in writing at the very least). Make sure you specify it is your domicilium address that you are changing – “A change in residential address does not serve to change a domicilium address.”

- And don’t think that your obligation to notify a change of address falls away once the contract is terminated. On the contrary, “the domicilium address survives cancellation of the agreement.”

End result – the judgment stands and the debtor must cough up.

Keep proof!

First prize of course is to avoid any disputes with the other party in the first place, but bad things happen to even the most careful of us so make sure that you aren’t left blissfully unaware of any notices or summonses that are issued against you at the wrong address. And if you do find yourself applying for a default judgment to be set aside, make sure you have kept proof that you notified the other party of your change of domicilium in the specified format.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“…sending bank details by email is inherently dangerous, and so must either be avoided in favour of, for example, a secure portal or it must be accompanied by other precautionary measures like telephonic confirmation or appropriate warnings which are securely communicated.” (Extract from judgment below)

Before you make any payment to a supplier’s bank account on the basis of an emailed invoice, check that the bank account details in the invoice are genuine.

If your supplier’s or your email system have been hacked in a BEC (“Business Email Compromise”) scam, the invoice details could easily be fraudulent and if so you will be paying into a scammer’s bank account.

Property transactions are prime BEC targets, but not the only ones!

You will have seen many warnings about the global problem of conveyancing email scams, where emails are intercepted and false bank account details appear in invoices or in the mails themselves. Property sales are usually high value transactions and thus a natural target for fraudsters.

Increasingly though, other non-property related business-to-business and business-to-customer transactions are being targeted – the higher the value of the deal, the more likely it is to be subjected to online crime.

Let’s take a topical example…

It’s high-value inverter time, and the bad guys are taking note…

You decide to install a high-value inverter, courtesy of Eskom’s “no end in sight” loadshedding. Inverter installers – let’s call them “Speedy Sparkies Inverter Systems” – email you a quote for R145,000. You accept. Back comes an emailed invoice from fred@speedysparkies.co.za asking you to pay R100,000 upfront to cover materials. You transfer R100k to the X Bank account on the invoice and ask when they will install. The friendly return email reads “Thanks for the payment, we’ll fit you in next week Thursday. Best, Fred”.

Thursday rolls around but no Fred. You phone him. “But you haven’t paid us yet” says Fred. “Yes I have, I paid into your account last week and you emailed confirmation of receipt of payment”. “No, definitely no payment received and no email from us confirming receipt.” “That’s impossible Fred, I have your email in front of me”. At which stage you notice, with a sinking heart and rising panic, that that last email came from fred@speedy-sparkies.co.za – with a hyphen. “Nope, really sorry” says Fred, “there’s no hyphen in our email address and we bank with Y Bank not X Bank. You’ve been scammed. We’ll try to help you but you need to pay the R100k again before we can install”.

Denial, anger, acceptance, then off to the bank to ask for help and off to SAPS to lay charges. Your bank and the police are sympathetic but not hopeful of recovery. So what happened?

How did you just lose R100k?

Using phishing tactics, the scammers hacked into Speedy’s email system then monitored all their emails, waiting for a high value contract to pop up. They pounced, intercepted the email to you with the invoice, changed only the return email address and the bank account.

You suspected nothing – the look and feel of the email and invoice are totally genuine, the wording of the mails is Fred’s (right down to his trademark sign-off “Best, Fred”), the email address difference is so subtle you don’t notice it. Sometimes scammers can even “spoof” an email address, where the sending email address appears to be the same as the legitimate one.

It all looks 100% authentic and of course by the time you and Fred realise anything is amiss, your money is long gone.

The only winners here are the scammers and the question now is “who is the loser?”

Who takes the loss? Who pays for your inverter now? Can you sue?

Here’s the rub – you blame Speedy for allowing their system to be hacked. You accuse them of negligence and of failing in their duty to keep your data safe in compliance with POPIA (the Protection of Personal Information Act). But Speedy deny fault and say you carry the risk and anyway it’s your mistake for not noticing the falsified email address and for not phoning Fred to check the bank account details. Speedy’s insurers confirm they have no cover for this sort of fraud.

Do you have a legal claim against the business? There’s no cut-and-dried answer to that, with our case law outcomes to date tending to vary with each particular set of facts, and the courts referring to various questions of proving negligence, compliance with payment instructions, “considerations of legal and public policy”, and reference to a general rule that anyone making a payment to someone else is required to check that they are paying into the correct account.

So as a customer, it’s probably safest to work on the basis that you could well be held to be the party at risk and will almost certainly have to prove (at the very least) negligence on the part of the business in order to stand a chance of establishing any claim against it.

As a business on the other hand, your legal position is far from secure. You will be accused of negligence (and perhaps also breach of POPIA) if it is your system that was hacked. Even if it is your customer’s email account that has been hacked you are still at risk, as confirmed by the recent High Court award of R5.5m (plus interest and costs on the punitive attorney and client scale) in just such a case against a conveyancing firm on the basis of its legal duty of care towards a property purchaser, and on a finding that “but for the negligent transmission of its account details and failure to warn [the buyer] upfront of the inherent danger of BEC, she would not have suffered the loss.” In the Court’s words “sending bank details by email is inherently dangerous, and so must either be avoided in favour of, for example, a secure portal or it must be accompanied by other precautionary measures like telephonic confirmation or appropriate warnings which are securely communicated”.

On a strictly practical level, your reputation is at stake and those 5-star Google Reviews could be in for a knock.

Bottom line – take legal advice specific to your case. Perhaps you will both be advised to cut your losses and to share the pain 50/50. Far from ideal, but a lot better than protracted and bitter litigation.

Prevention being as always a lot better than cure, we share below some ideas on how to protect yourself from this sort of cyber fraud in the first place.

Prevention – here’s what to do

- Businesses: Most importantly, protect your systems from being hacked! Train all staff in the increasingly sophisticated nature of phishing emails, update all your software and beef up your anti-virus and anti-malware protections and protocols. Consider not putting your banking details on invoices and tell customers to phone you to check any details they are given. Consider using a secure payment portal with two-factor authentication (2FA) and protect any PDF documents you send (it’s a myth that PDFs can’t be altered). Tell customers on every email that you will never advise any change of bank details by email. Check with your insurers whether you can get cover for this risk.

- Customers: Take the same strong anti-hacking measures. Never pay anything without checking bank details direct with the business, either in person or telephonically (don’t use the phone numbers on the emails or invoices, they could easily have been faked as well). Check email addresses carefully – make sure the return address is the same as the sender’s address (some tips on how to do that here), watch for subtle changes like ‘.co.za’ becoming ‘.com’ or vice-versa, and remember that every hyphen, every letter and every number in the email address counts. Use bank-defined beneficiaries for online banking where possible. Be very suspicious of any “we’ve changed our banking details” communications.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“Finally, we pay tribute to the millions of South Africans, whose resilience and courage during these times of pandemic and economic hardship, is an inspiration to all of us who have the privilege to serve in the public sector.” (From the 2022 Budget Speech)

Finance Minister Enoch Godongwana has invited the public to share suggestions on the 2023 Budget he is expected to deliver on Wednesday 22 February 2023.

Go to National Treasury’s “Budget Tips for the Minister of Finance” page and fill out the online form.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

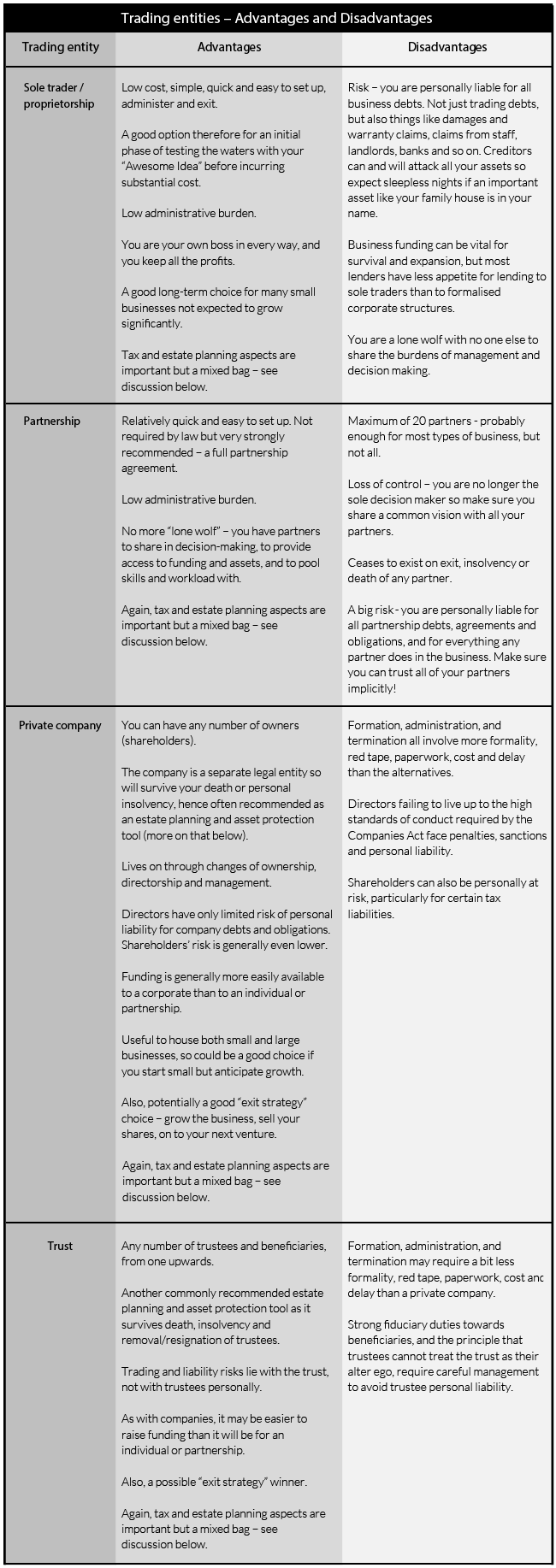

“Owning one’s own business is an adventure – enjoy it every step of the way.” (From the SME Toolkit article referenced below)

First, three questions to ask yourself…

If you dream of going into business for your own account in 2023, ask yourself these questions before you get started –

- Am I an entrepreneur? You have an amazing idea, you can’t wait to launch your new business, success and wealth beckon! But wait a second – are you really suited for the hurly-burly of entrepreneurship? It can be hugely rewarding, not just in the financial sense but also in terms of lifestyle and life satisfaction. But it also carries far more risk than the classic “9 to 5 employee” option, so think long and hard before choosing. There are many online quizzes to help you decide – try for example DeLuxe’s “Quiz: Are you ready to start your own business?” here.

- What’s my plan? Without a plan you sail rudderless through some very treacherous and shark-infested waters. Start-up failure rates are high, but luckily there is plenty of advice available to help you plan your course. Read for example the Business Partners “Ten Simple Rules For a Successful Start-up” on SME Toolkit.

- What legal entity should I use to trade? Don’t make the rookie mistake of setting sail in just any old boat. Starting off in the wrong entity and then having to change mid-stream will mean a lot of unnecessary expense, hassle and risk. Rather plan long term – ask yourself where you want your business to be in 5 or 10 years, how big it will be, what your exit plan will be and so on.We set out below some brief thoughts on the various alternatives available to you, but upfront professional advice, specific to your particular needs and circumstances, is a real no-brainer here.

So, what are your choices?

…and four business vehicles to choose from

You have four main options –

- A sole proprietorship (“sole trader”). You are the business, trading for your own personal profit and loss, perhaps under a trading name such as “Syd Smith trading as ‘Syds Plumbing’”.

- A partnership of 2 to 20 individuals or entities, pooling resources to carry on a trade, business or profession for a share of the profits.

- A private company (“Pty Ltd”) with any number of shareholders. Controlled and administered by directors.

- A trust (number of trustees and beneficiaries not restricted). There are various types of trust, with trustees controlling and managing trust assets and/or trading for the benefit of beneficiaries.

Note that you might be advised to combine one or more of these entities in a corporate structure, and that there are other specialised types of entity available to, for example, non-profit organisations (charities etc), professionals (lawyers, accountants, doctors etc) and the like.

The pros and the cons of each

Have a look at the illustrative table below for a summary of the advantages and disadvantages of each of these options.

Don’t forget the tax and estate planning implications!

Each of your choices carries with it a mixed bag of positives and negatives when it comes to both tax and estate planning implications. For an overview, have a look at SARS’ “Starting a business and tax” webpage, with a link to its “Tax Guide for Small Businesses” PDF.

That Guide is 102 pages long, and unless you are comfortable with the complexities involved, professional advice specific to your circumstances is again essential.

In a nutshell –

- Estate planning: You may be advised to use companies and trusts for tax-efficient and practical transfer of wealth to future generations, as well as for asset protection from creditors both before and after you die. Both companies and trusts are “perpetual” in the sense that they survive changes in directors/trustees (resignation, removal, retirement, insolvency, death etc), with potential multi-generational savings in estate duty and avoidance of the cost and delays inherent in deceased estate administration.

- Tax efficiency: Sole traders and partners are taxed at individual rates; trusts other than special trusts at a flat rate of 45%; companies at a flat rate of 27% (27% for years of assessment ending on 31 March 2023 and later, previously 28%) with 20% dividends tax when you take profits out. There are a host of other factors to take into account here, including aspects such as Capital Gains Tax inclusion rates, exclusions, exemptions, small business breaks and the “trust conduit principle” all being highly relevant to the ultimate question – will you be better off being taxed as an individual or will some form of corporate and/or trust structure be more tax efficient for you?

Take that professional advice!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNew