“It would thus be prudent that a commercial lease agreement includes a clause dealing with the risk associated with vis maior, casus fortuitus and the impossibility of performance.” (Extract from judgment below)

The Covid-19 pandemic and its associated lockdowns and restrictions have impacted negatively on many businesses, and there has been much uncertainty as to whether commercial tenants of leased property are entitled to claim a remission of rental if their trading activities are curtailed.

A recent High Court decision throws some light on this knotty question, and with the pandemic showing no signs of letting up, all commercial landlords and their tenants should be aware of it.

The steakhouse closed by lockdown regulations

- The Greenpoint Butcher Shop and Grill, a “well-known premium steakhouse restaurant”, was forced to close during the “hard lockdown” period.

- Sued by its landlord for just under R3m in arrear rental, the tenant raised as one its defences that the lockdown regulations had closed its doors for the duration of the hard lockdown, with only reduced trading possible as restrictions thereafter eased. This had rendered it impossible for it to perform its obligations in terms of the lease, plus “a supervening event made performance impossible and thus there was thus no beneficial use of the leased premises for the purpose for which it was intended.” The landlord, it said, had been unable to give it “beneficial occupation” and it was entitled to a remission of rental accordingly.

- The landlord replied that in terms of the lease, all amounts due had to be paid “free of deduction and set-off”, the tenant’s problems arising from the lockdown regulations did not excuse it from paying rental, and the full amount was still due.

- Before we get to the eventual outcome of this case (spoiler alert – it doesn’t end well for our unhappy tenant) the Court’s analysis of our law on the matter provides some useful and practical advice for both landlords and tenants.

Firstly, let’s understand “the Latin bits”

Apologies for inflicting legalistic Latin terms on you but a basic understanding of these two is important for landlords and tenants, particularly as you may well come across them in the Ts and Cs of a lease in the context of “supervening impossibility of performance” –

- Vis maior (or vis major), means ‘superior force … some force, power or agency which cannot be resisted or controlled by the ordinary individual’.

- Casus fortuitus, or “inevitable accident”, is a type of vis major, which ‘imports something exceptional, extraordinary, or unforeseen, and which human foresight cannot be expected to anticipate, or which, if it can be foreseen, cannot be avoided by the exercise of reasonable care or caution’.

When is rental remission allowed?

- Our law is that “a lessor’s duty is to deliver the leased property in a proper condition and that the property is to be placed at the disposal of the lessee for its undisturbed use or enjoyment”.

- Thus the general rule is that, unless the lease specifically provides otherwise, a tenant can claim rental remission “where there is a deprivation of or lack of beneficial use or occupation …, partially or fully, of the leased premises, and where the interference is caused by vis maior or casus fortuitous, neither of which eventuality is the fault or cause of either the lessor or lessee”.

- Critically, the Court in this case held that “the COVID-19 regulations passed in terms of the Disaster Management Act would amount to vis maior or casus fortuitous” (emphasis supplied).

- A tenant can set off a rental remission against the landlord’s claim for non-payment of rental only “if it is capable of speedy and prompt ascertainment”.

- Each matter must be considered in light of all the facts – “the specific regulations applicable at the relevant time(s), the extent to which performance was not possible, the extent to which there was a lack of beneficial occupation (if any)” and the provisions of the lease. This last is a critical point – the tenant’s obligation to pay rental remains, even where the impossibility of performance is not due to his fault, “where the parties specifically provided in their agreement that the lessee would be responsible for and/or take the risk upon himself for the impossibility supervening” (emphasis supplied).

Which brings us to…

The sub-tenancy that sank this tenant’s defence

In the end however, the tenant was ordered to pay the full amount of rental outstanding.

Its problem was that it had effectively sub-let the premises to another legal entity. In a case of sub-lease, held the Court, the landlord’s obligations are towards the tenant, not towards the sub-tenant. The steakhouse being a sub-tenant, it could not claim rental remission from the landlord. Neither could the tenant claim remission of rental because it was not itself in possession and control of the premises. An appeal against this aspect of the judgment is pending.

As an interesting side note (which could be of use to you if you are a sub-tenant or have sub-let to one) there is much discussion in the judgment around an old 1902 Transvaal Supreme Court (TSC) case. A hotel had been forced to close after the government of the time had prohibited the sale of liquor by hotels and bars, and it had re-opened only temporarily when forced to house military forces during the war. The TSC allowed rental remission even though a sub-lease was involved, apparently on the basis that the tenant and sub-tenant in that matter were “one and the same”. In contrast, in our 2021 steakhouse case the tenant and sub-tenant were found to be totally separate legal entities, so the 1902 case was in the end of no help to the tenant. Nevertheless the principle has been established that in certain cases a sub-tenant may be able to argue for remission.

The Court’s advice to commercial landlords and tenants

As the Court put it: “It would thus be prudent that a commercial lease agreement includes a clause dealing with the risk associated with vis maior, casus fortuitus and the impossibility of performance.”

Landlords – have your leases checked immediately to ensure that you are covered against any possible rental remission claims.

Tenants – you will want to negotiate any such clause to give you some leeway should disaster strike. Otherwise be ready to bear the consequences if the pandemic (or indeed any other unforeseen disaster) should suddenly force you to close your doors. Think also of tying this in with some form of business interruption insurance.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“All is fair in love and war…and business is war.” (Jasmine Kundra)

When company directors are locked in dispute, one of them may be tempted to cut off the other’s access to emails and to the business server – a tactic likely to have immediate and serious consequences for the director thus cut off.

Its appeal as a tactic to force the other director to the negotiating table is obvious, but the question is whether the director thus deprived has any legal remedy available to force immediate restoration of access.

A recent Supreme Court of Appeal matter saw a director in that exact position trying to get his access back urgently with a “spoliation order” application.

“Cut off his email and server access”

When the two directors fell out, one (let’s call him ‘A’) applied for liquidation of the company on the grounds of deadlock. Director B opposed this application, and, alleging that A had resigned his directorship, instructed the web hosting entity hosting the company’s server and email addresses to cut off A’s ‘email and company network/server access’ with immediate effect.

A, denying hotly that he had resigned, immediately applied to court for a “spoliation order” restoring his email and server access to him.

Spoliation – a quick and effective way to get back possession, but only if…

- The spoliation process is designed to stop disputing parties from taking the law into their own hands and provides a quick and effective way of regaining possession of something if you have been wrongfully deprived of it. It’s a quick and effective remedy because “[T]he injustice of the possession of the person despoiled is irrelevant as he is entitled to a spoliation order even if he is a thief or a robber. The fundamental principle of the remedy is that no one is allowed to take the law into his own hands”. In other words, you can get an immediate spoliation order without having to prove your right to possession of the thing – all you have to prove is the wrongful dispossession.

- So that would have been an ideal outcome for A, giving him immediate restoration of his access to his emails rather than having to fight his way slowly through a full trial proving his rights to email and server access. But it was not to be. His problem was that, in order get a spoliation order, one of the first things you must prove is that you were in “peaceful and undisturbed possession” of something.

- Now A would have been able to prove such possession if he had for example been wrongfully deprived of use of a company car or even of an “incorporeal” right to use property (such as “quasi-possession” of a right of access under a servitude). But he was unable to convince the Court that his email/server access fell into any such category.

- As the Court put it: “Thus only rights to use property, or incidents of occupation, will warrant a spoliation order.” A’s prior use of the email address and server was not an “incident of possession of movable or immovable property”, it is purely “a personal right enforceable, if at all, against [the company].”

- In a nutshell, A must now prove his legal right to email and server access – perhaps he will be advised to apply for an ordinary interdict, perhaps he will sue for damages and/or re-instatement, but whichever course he chooses he will need to accept the inevitable delays. In other words, if B’s tactic was to put immediate and substantial pressure on A in the short term it worked – at least for now.

Don’t however take any action like this without professional advice – it could come back to bite you badly if it misfires.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

Even if your marriage is collapsing around you, you might be afraid to sue for divorce because you have no money to survive on, plus you know that a hotly contested divorce might take years to finalise while your breadwinner spouse fights you tooth and nail every step of the way.

How will you support yourself and your children until the case is finalised? How will you pay your lawyer to run the case for you? Must you wait for the end of the case before you see a cent?

The answer luckily is “no” in that you have a relatively quick and simple remedy in the form of asking the court for “interim relief” in respect of –

- An order that your spouse pay you –

- Maintenance (for children and/or for yourself) pending finalisation of the divorce,

- A contribution towards your costs in the divorce proceedings,

- Interim care of, and contact with, your children (if there is any dispute over this aspect).

You may well hear this form of relief referred to in High Court divorces as a “Rule 43 application” (or, if your divorce is in the Regional Court, as a “Rule 58 application”), whilst the technical term for the maintenance is “maintenance pendente lite” (“maintenance pending the litigation”).

At this stage the Court isn’t interested in recriminations, or blame-finding, or the itemised details of your and your spouses’ financial positions. Those enquiries come later, during the actual divorce litigation. At this stage all it wants to know is how much you need, and how much your spouse can afford to pay.

A recent High Court judgment illustrates…

A “coy about his wealth” spouse ordered to pay up – now

- The warring spouses here are a senior banking executive and his wife, who qualified as a teacher but gave up that career to become a homemaker and mother to the couple’s two children.

- She asked the High Court for interim maintenance for herself and the children, and for a contribution to her legal costs.

- In assessing these requests the Court laid out some of the general principles involved –

- Unless the care and residence of children is involved the issues are straightforward, relating to “the applicant’s reasonable needs, and the respondent’s ability to meet those needs. The applicant’s entitlement to maintenance must be assessed having regard to the standard of living enjoyed by the parties during the marriage.” This should be “a simple and straightforward calculation of needs and means”. (Emphasis supplied).

- The aim is “to avoid substantial prejudice to either party pending divorce. It is not to provide a precise account of what is due to or from either party, according to the parties’ or the court’s sense of morality, propriety, the blameworthiness of the parties’ conduct during the marriage, or their habits of living after the separation.” The case should be cast in practical rather than moralistic terms, and the “emotional heat of a separation” should be kept out of it.

How much money could you be awarded?

Of course every case will be different, but where the parties have, as in this case, enjoyed a high standard of living, the figures can be substantial.

Here for example the Court’s awards were sizeable, commenting that the husband “is coy about his wealth, but there is little doubt that he has a substantial income” – just under R7m in the previous year – with “considerable resources” and an estimated net worth of just over R40 million. Moreover the couple had enjoyed “a very comfortable lifestyle” together.

The end result is that the husband must pay substantially what his wife asked for in the form of R1.6m immediately and thereafter R108k p.m. –

- R88,701-69 p.m. for the wife and children’s interim maintenance, plus school fees, extra mural activity costs, medical aid and medical costs

- Rental of up to R20,000-00 p.m., plus cost of utilities

- R34 656.39 for house moving costs

- R1,572,945-80 as a contribution towards the wife’s interim legal costs.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“…sexual harassment is a heinous and horrendous conduct since it undermines the dignity of women and the values enshrined in our Constitution.” (Extract from judgment below)

Employers have a strong duty to provide a safe workplace for their employees, and to protect them from harm – including sexual harassment. An employer who fails in this faces claims for damages and compensation, but as a recent Labour Court judgment shows, the victim must first follow procedure correctly, and without delay.

Delayed reporting kills a claim

A female employee claimed “a just and equitable compensation” from her employer after she was sexually harassed by two male superiors.

Her claim failed, the Court finding that her delay in reporting the incidents to her employer (two years in one case and three in the other) were……

The correct procedure, and the required timing

The employee’s claim was based on an allegation that her employer had contravened section 60 of the Employment Equity Act (EEA), which deems an employer guilty of a contravention and liable for the offending employee’s conduct unless it takes “the necessary steps to eliminate the alleged conduct and comply with the provisions of this Act” and “is able to prove that it did all that was reasonably practicable to ensure that the employee would not act in contravention of this Act.”

The Court set out the required steps by the victim as –

- Allege a contravention at the workplace

- Report the contravention immediately

- Prove the alleged contravention

- Allege and prove failure to take the necessary steps.

A victim who can prove all the above is entitled to a deeming order of liability, and to avoid liability it is then up to the employer to prove that it took the necessary and preventative steps.

The victim in this case had no trouble in proving that the incidents of sexual harassment had taken place, but she failed to convince the Court that she had brought the incidents to her employer’s attention “immediately” as required by the section. The Court referred to a previous decision of the Labour Appeal Court suggesting that the word “immediate” be given a “sensible meaning”. In that case a two-month delay in reporting was found to be acceptable as a “limited delay”. However the Court’s comment that “In my view, a delay is an antithesis of the word as literally defined” is a clear warning to victims – report incidents to your employer without delay!

In any event, held the Court, the victim’s delays in reporting (two and three years respectively) meant she had failed to report “immediately” as required.

The Court was equally unimpressed with her suggestion that she had indeed reported the incidents to her employer in time by discussing them with “colleagues and managers”. That, held the Court, was not enough: “As I see it, to my mind, the reporting must be to an employer through the mechanism in its adopted policy.” She had not done that, so there’s another clear lesson for victims there – make a formal report to the correct person/s in terms of your employer’s policies.

Finally, said the Court, the employer had as soon as it received the reports, promptly investigated them and complied with its obligations in terms of the EEA.

Claiming from the offenders themselves

On a related note the Court mentioned that the victim would have a claim direct against the two employees who harassed her. Once again however, time is of the essence for victims – quite apart from the risk of the claim prescribing, the earlier formal reports are made the greater the credibility likely to be given to them.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

Being an entrepreneur can be hugely rewarding, but it comes with a level of stress at the best of times, now magnified many times over by the pandemic’s uncertainties and disruptions.

Of course stress can be good for us, but only up to a point. “Bad stress” won’t just damage your ability to run your business, it puts your mental and physical health at severe risk.

So whatever else you do this year, make sure that coping with stress is high on your agenda – very high. Get 2022 off to a great start with these stress-coping mechanisms from a team of clinical psychologists on Stuff.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“Luck is what happens when preparation meets opportunity” (Lucius Annaeus Seneca the Younger, Roman philosopher)

History has not recorded whether Seneca himself was “lucky” in the property market of his time (Rome’s land registration records from two millennia ago have unfortunately not survived the ravages of time and Imperial collapse) but his wise words are as true today as they were then.

The two key elements of a “lucky” sale

To be “lucky” in finding the right buyer at the right price you need two key elements –

- Opportunity: Our Holiday Season is always a prime time to find the perfect buyer, and with our current low interest rates, local and international travel opening up again, and reports of house prices soaring globally, December promises to provide plenty of opportunity to sellers; and

- Preparation: We have some useful tips for you here, both from a legal standpoint and from a practical one…

How to prepare for a “lucky” house sale in 12 steps

First prize is of course a quick sale at a good price, followed by a smooth transfer process. Here are some thoughts on how to achieve exactly that –

- The sale agreement – avoiding the legal pitfalls: Your house is probably one of your most important assets, so be aware of and prepare for the many legal pitfalls which may await you. Falling into any one of them could instantly convert your “lucky” sale into a disaster!Note firstly that as seller you have the right to choose your own conveyancing attorney. Do not fall into the trap of giving that right up! Pick someone you trust to carry out the transfer (the formal registration in the Deeds Office of the property into the buyer’s name) quickly and professionally.You will be bound by all the terms and conditions in the sale agreement you sign, and there are far too many potential pitfalls here to list in one article. So have your own attorney prepare the offer/sale agreement for you, and if you happen to be presented with an offer on someone else’s offer form, at least have your attorney check it for you before you sign anything.Every term and every condition, no matter how “standard” it may seem, must be scrutinised to confirm that it suits your particular sale and your particular needs. Common things to go wrong include badly worded “voetstoots” and “bond clauses”, uncertainty over payment provisions, confusion over the authority of company directors and trustees of trusts to sign agreements and so on.

- Well in advance… Pick your attorney’s brain on a few preliminary (but deeply important) aspects like which estate agent/s to use, what sale prices are being achieved in your area and who is buying, and so on. Ask also for a list of what your costs are going to be, when you are likely to get paid the purchase price etc so you can prepare a cash flow forecast. Get a start with all your compliance certificates and provide for the cost of any remedial work needed (normally on the electrical and plumbing side). You may also have to give up to 90 days’ notice of cancellation of your home loan to your bondholder to avoid an early termination fee – check with your bank.

- Time it right: If you are selling a house – “holiday home” or not – in a traditional “holiday” area, the Festive Season will likely be your prime selling time. Sunny weather, everyone relaxed and in the holiday spirit, an influx of holiday makers from other cities – they all set the scene for you to show off your home to best advantage and to the best audience. Which brings us to…

- Describe and target your “perfect buyer”: Sit down with your family/friends/professional advisors and brainstorm who your “perfect buyer” is. Who will want your house the most? Who is going to pay you the most for it? Perhaps for example you come up with a spec like “Our perfect buyer is a young upwardly-mobile family looking for work-from-home-space, good schools in the area, and a separate flatlet for Granny.” Use that spec to inform your “market targeting” – how you plan to reach that target market, how you will tell it just how perfect your home is for them, and so on.

- Set the right asking price! A very common mistake, and an easy one to make, is over-pricing. Maximise buyer interest and engagement by asking for a reasonable, market-related price. With of course a margin for negotiation. Get good independent advice here – we tend to be very emotionally invested in our own “home-sweet-home” and it’s not easy to be objective about its attractiveness and value to outsiders.

- Advertising: Your first challenge is to get “feet through the front door” so unless you are very confident indeed of your own ability to find the right marketing channels and formats, professional advice and guidance is essential here! Remember that “a picture paints a thousand words” so bringing in a professional photographer is a no-brainer. You could seriously damage your home’s image in the public mind if you take a chance and get any of this wrong at the start.You want to highlight your property’s strengths, particularly those likely to appeal directly to your target market (identified above), so think of all the easily-overlooked things like borehole water, irrigation systems, solar power, inverters, fibre, special security features, herb garden space – the list is endless.

- Prioritise kerb appeal: If you get the above steps right, sooner or later your perfect buyer will be arriving at your street address. Critical here is kerb appeal – the “attractiveness of a property and its surroundings when viewed from the street”. Don’t drop the ball on this one! “You never get a second chance to make a good first impression” said Will Rogers, and the same holds for your house. Ask some friends to drive down your street with a fresh pair of eyes – what jumps out to them as appealing? What could put a potential buyer off?

- Now comes “front door appeal”: So your perfect buyer now stops the car, decides to give your property a look-over, and parks – great going! Into your front garden we go – is the lawn cut and lush, trees and shrubs tidy, flower beds bursting with colour? Is the house exterior attractive, the paint job and roof in good condition? Does your entrance/front door shout “come on in”?

- Light, clean and airy sets the scene: We’re inside, now what’s the first thing your potential buyer will see? A bright, spacious, airy feel could seal the deal right there and then, whilst even the slightest trace of dim, musty airlessness could kill it stone dead. Whatever issues you identify, there is a treasure trove of advice on the internet about how to address them – lighter wall paint and curtains, more natural light from outside (a big seller!), sparkling windows, more interior lighting, a few mirrors to give a feeling of light and space, de-cluttering, re-arranging the furniture – your own house’s strong and weak points will be unique to it. Finish off with a really deep clean, calling in the professionals particularly if the house is old, if you have pets or have just got rid of old dust-gathering clutter.

- Deal maker kitchens and bathrooms: Your kitchen and bathrooms could be deal-makers, or they could be deal-breakers. More than perhaps any other area of your house, they are worth spending money on if they haven’t got immediate appeal already.

- Work-from-home office space: Depending on who you have identified as your “perfect buyer” in step 2 above, this could be critical. If you don’t have an office/study already set up, identify a space for one and be ready to answer questions like “do you have fast fibre?” and “how noisy are your neighbours?”

- The DIY factor: Unless your plan is to sell a “fixer-upper with huge potential and in need of a little TLC”, have a good look around for all the “little things” that need fixing (we’re outside as well as inside the house now) – cracked tiles, broken fittings, leaking taps, a grubby swimming pool – anything really that a prospective buyer might notice and think “I wonder what else is wrong here?”

Bottom line – make your own luck!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“… it is by now long established in our law that the owner or other person or entity in control of a shopping mall has a legal duty to take reasonable steps to ensure that its premises are ‘reasonably safe’ for those members of the public who might frequent them … What such steps may be will depend on the circumstances.” (Extract from judgment below)

The Festive Season is once more upon us, cueing shops, shopping centres and malls packed with ever-growing crowds of shoppers.

What happens if you fall while shopping and hurt yourself? Our law reports are full of cases where shops are sued for damages following “slips” and “trips”, and a recent High Court case confirms once again that as a general rule shops and malls are liable to keep their visitors from harm.

A broken elbow from a slip on a wet mall floor

- A shopper visited a mall to draw money from an ATM on a rainy day. Rain carried into the mall by other shoppers on their rain jackets, umbrellas and shoes had left the floor wet and slippery, and she saw a yellow ‘wet floor’ warning sign on the tiled floor.

- 14 metres from the mall entrance her feet suddenly gave way from under her and she fell, extending her right arm to break her fall and shield the baby she was carrying. She was left with a fractured elbow.

- She successfully sued both the mall’s owner and its management company for damages, a “Full Bench” of the High Court ordering the two companies to pay “jointly and severally” whatever damages she can prove.

- “Thus, in summary” held the Court, “the owner or person or entity in control of a mall will only potentially be liable for harm or danger which would have been foreseeable to the hypothetical reasonable man in its position, and is obliged to take no more than reasonable steps to guard against such harm occurring … Whether the steps that were taken in a particular case are to be regarded as reasonable or not depends upon a consideration of all the facts and circumstances, and merely because harm which was foreseeable did eventuate does not mean that the steps which were taken to avoid it were necessarily unreasonable. Ultimately the inquiry involves a value judgement on the part of the Court.”

- The Court found that the “legal duty to take reasonable steps to safeguard the [shopper] from harm that day … was one which fell primarily and squarely” on the owner and its management company.

- It rejected the defence raised that the mall’s cleaning contractors were the liable party with the comment “It would be a startling state of affairs if independent cleaning contractors in shopping malls who are only contracted to keep floors clean became saddled with a duty to safeguard those who frequent the mall premises, and became liable to them on this basis in the event that they failed to comply with their contractual cleaning duties.”

What about “enter at your own risk” disclaimer notices?

Another defence raised was that there were “enter entirely at your own risk” type disclaimer notices “prominently displayed” at all entrances to the mall. The shopper denied having noticed any such notices either on the day in question or on previous visits to the mall, and the Court found that the mall owner and manager had failed to prove that –

- Such a notice was displayed at the time, and

- The shopper had read and accepted the terms of the notice “or at the very least that they had taken ‘reasonably sufficient’ steps to ensure that the notice would come to her attention in the ordinary course”.

The bottom line for shop and mall owners

Take all reasonable steps to keep your visitors from harm, and ensure that you have adequate and prominent disclaimer notices displayed at all times. Keep these notices updated – one of the mall owner’s problems in this case was that the disclaimer notices were old and still in the name of a previous owner.

The bottom line for shoppers

As this judgment shows, you have to jump through a number of loops to establish a claim. Besides, shops and malls by their very nature present dangers to the unwary – spillages, items dropped on the floor, wet and slippery surfaces and the like are common and if you don’t keep your eyes open and your wits about you, you run the risk of a court holding you fully or partially liable for your own misfortune. In that event it could dismiss your claim or at most only award you part of your damages on the basis of your “contributory negligence”.

Worse, you could have no claim at all if a court finds you bound by an “enter at your own risk” disclaimer sign.

So – enjoy your Festive Season shopping, but Safety First!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“Someone’s sitting in the shade today because someone planted a tree a long time ago” (Warren Buffett)

Whilst the first and most important step in your estate planning is always to have in place a professionally drawn and regularly updated will (“Last Will and Testament”), there is another aspect which demands your urgent attention, particularly now…

What will your family live on while an executor is being appointed?

It is essential that you provide for your family’s ongoing financial needs during the process of winding up your estate, because all your bank accounts will be frozen as soon as the bank learns of your death, pensions and the like take time to transfer across, and your assets generally will be tied up in your estate and inaccessible to your loved ones.

The executor of your deceased estate does have the power, provided of course that your estate is solvent and has sufficient funds, to release money to your dependents and to make advances to your heirs – but only after being formally appointed. Which brings us to…

Delays in the Master’s Office are getting worse

No matter how professional and efficient your nominated executor may be, he or she is powerless to act until the local Master of the High Court (“Master’s Office”) issues the necessary “Letters of Executorship” (“Letters of Authority” in smaller estates), so applying for them is always a priority for those nominated.

The issuing process has never been a quick one, but delays have worsened substantially in the past few years with media stories abounding of major problems in Master’s Offices around the country and reports of “unprecedented backlogs” and “an almost total breakdown in services”.

The recent ransomware attack on the Department of Justice and Constitutional Development is just the latest in a litany of woes afflicting these offices – pandemic-related lockdowns, office closures and remote working, staff shortages and a surge in the number of deaths, a Special Investigating Unit investigation into allegations of misconduct and corruption in some offices (with two officials suspended so far and many others reportedly in the firing line) – the list goes on.

Nominated executors are complaining of inordinate delays in being appointed, and of extreme difficulty in communicating with Master’s Office officials by phone, email or even by personal office visits.

Here’s how to fund your loved ones in the interim

The bottom line is that you will leave your grieving family dealing with financial worries at the worst possible time if they have to wait for your chosen executor to be appointed.

You need to find another way of giving them immediate access to funds, enough to cover their living expenses and any new expenses like funeral costs.

There are a few tried and tested ways of providing this cash flow, with separate bank accounts and investments being probably the simplest and most quickly accessible options. Consider also other assets in family members’ own names, family trusts, businesses held in entities that will survive your death, and so on. Another popular choice is life/endowment policies, TFSAs (Tax Free Savings Accounts) based on a life product, living annuities and the like – be sure to nominate beneficiaries for these products otherwise they will fall into your estate and not be paid out to your loved ones direct. Be certain that your loved ones know what measures you have taken and how they can access these funds quickly and easily.

Your own situation will be unique and you need to structure everything correctly, so there is no substitute for professional advice here!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

“A man who procrastinates in his choosing will inevitably have his choice made for him by circumstance.” (Hunter S. Thompson)

Since 2005 businesses have been repeatedly told “get your PAIA (Promotion of Access to Information Act) manual sorted now, the deadline is approaching”. And every 5 years since then, those (mostly smaller) businesses temporarily exempted from lodging manuals have been given yet another extension – usually at the very last minute.

“Crying Wolf” again?

With government “Crying Wolf” so often, small business owners can certainly be forgiven for treating this whole process with a great deal of scepticism. Perhaps though this deadline is one to take seriously, particularly since the related POPIA (Protection of Personal Information Act) is now fully in place and new PAIA Regulations have been promulgated to tie in with POPIA.

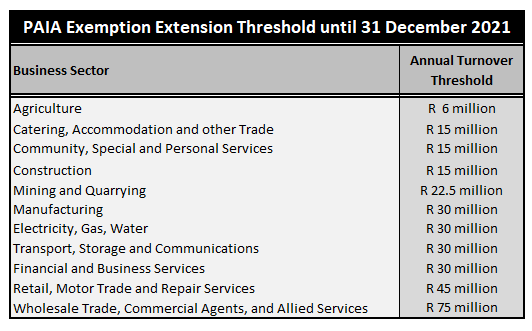

What businesses are currently exempt?

PAIA itself requires all public and private bodies to prepare, lodge and publish (including on any website you have) a PAIA information manual. Every business operation, no matter how small, falls into that net – the definition of “private body” includes any person or partnership who carries on or has carried on “any trade, business or profession”, together with any “former or existing juristic person” and political parties.

In other words, all businesses of all types and sizes must have a PAIA manual once the current exemption comes to an end.

You are probably currently exempt if you are a smaller business, specifically a “private body”, including any private company.

But the exemption does not apply to any non-private company, nor to any private company in any of the business sectors listed below with either –

- 50 or more employees, or

- An annual turnover of or above specific thresholds – see the table below for details.

Do your Manual now anyway!

Even if the deadline is once again extended, you will almost certainly still have to comply somewhere down the line, and at least by getting this done now you have got rid of one annoying little red tape item from your Action List. Procrastinating, as Hunter S Thompson pointed out, just means having the choice made for you down the line.

Prepare your PAIA manual now; if you already have one, update it regularly.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

Our cellphones have, for most of us, become integrated into virtually every aspect of our lives.

Take a moment now to think of how much damage a cybercriminal, or an industrial spy, perhaps even a malicious stalker or vengeful ex-employee, could do both to you personally and to your business if they succeed in getting spyware onto your phone.

Concerned? Firstly be aware that “spyware on your cellphone” is a real threat, and then act immediately to protect yourself.

A good start is this guide to –

- What spyware is,

- What the warning signs of infection are, and

- How to remove it from your mobile devices

Read “How to find and remove spyware from your phone” on ZDNet.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews